In 2022, the Federal Reserve launched an aggressive series of rate hikes to curb inflation at levels the U.S. had not experienced since 1979. The era of sub 3% 30-year fixed mortgages effectively ended, with rates climbing from below 3% to over 8% in less than 18 months, which are rates many people alive today may never see again. This sharp increase in borrowing costs disrupted the steady growth in single-family home sales, leading to a prolonged downturn. From November 2022 through November 2023, home sales fell for 13 straight months.

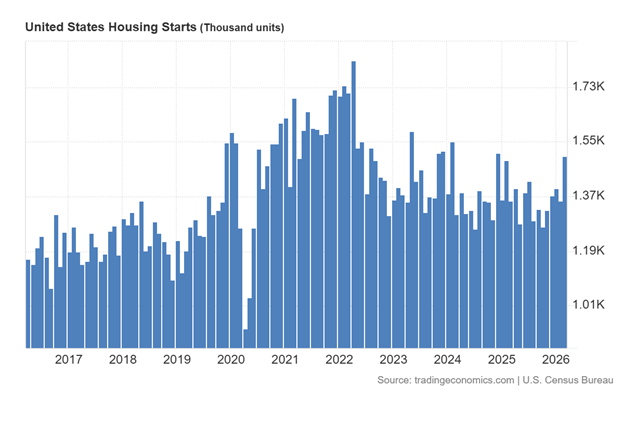

Meanwhile, in 2020, homebuilders ramped up new development projects to meet surging demand as buyers moved away from dense metropolitan areas in search of more suburban space. Unlike buyers, however, contractors can’t quickly pivot when market conditions change. While individuals can delay purchasing a first home or upgrading, builders are committed to long-term projects already underway.

After 2022, the cost of homeownership rose sharply, with affordability worsening by nearly 300%, driven largely by higher mortgage rates. This created a difficult situation for builders: construction pipelines were still full just as demand began to cool. Because new developments require years of planning, land acquisition, and permitting, it’s not easy to slow or halt progress once construction begins. The result was a growing imbalance as housing inventory increased while buyer activity declined.

By the end of 2022, construction of new housing had plummeted from a peak of 1,820,000 new houses in April 2022 to 1,300,000 by December 2022.

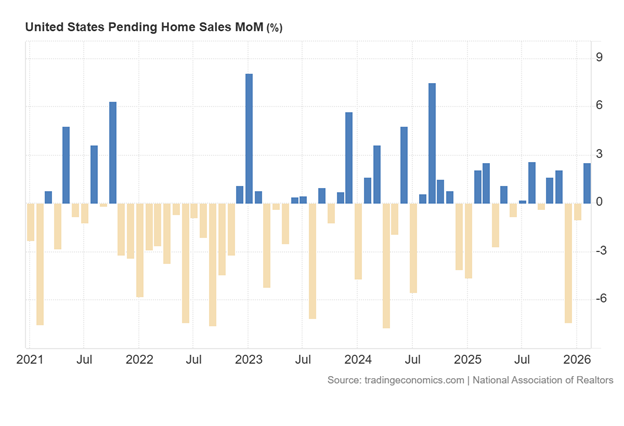

Even though the imbalance of supply and demand seems to be stabilizing, home affordability has only slightly improved since 2023. Mortgage rates are still above 6%, and home prices have continued to rise at a moderate pace. We do not expect material changes in home prices or mortgage interest rates.

As of December 31, 2025,DoorLoop.comreported that national homeownership was 65% vs 35% for those renting as of 12/31/25. The national rental vacancy rate is 7.0% vs 6.6% a year earlier. The median national rental asking rate is $1,494, and median asking home prices were $346,700, and median existing home prices were approximately $412,000 to $427,000. Lastly, first-time home buyers were down to a historic low of 21% of home purchases.

What Does This Mean to Me?

Consumer spending accounts for roughly 66% of total U.S. economic activity, and housing remains the largest expense for most households. Although the housing market has experienced slower activity, overall consumer spending has continued to show resilience.

In addition, approximately 70% of S&P 500 companies reporting earnings have exceeded analyst expectations and issued constructive guidance for the second quarter of 2026. Businesses and those particularly within the technology sector continue to forecast healthy growth in revenues and net profits. According to the Bureau of Economic Analysis, overall U.S. corporations are projected to generate between $4.30 trillion and $4.45 trillion in annualized pretax profits in 2026.

Given these favorable economic and corporate fundamentals, we continue to maintain a positive outlook on both the U.S. economy and the stock market. Please feel free to contact us with any questions regarding this update or your personal financial planning needs.