In the year 578 AD, a construction company was founded in Osaka, Japan to build a Buddhist temple. That company, Kongo Gumi, is still operating today. It has been maintaining temples, including the very first one it built, for more than 1,400 years. If you’re wondering, the answer is yes, this is the longest running company that is still active.

Kongo Gumi is not alone. Japan is home to roughly 140 companies older than 500 years, and more than half of the world’s companies older than 200 years are Japanese. The Japanese have a word for these firms, shinise, and they are governed by written family principles handed down across generations. These family principles focus on the most important elements of building a longstanding business, which are non-negotiables and prioritize continuity. In no particular order they are to protect the core craft, avoid debt, accumulate reserves, and plan succession decades ahead.

When you buy from a shinise, you are not really buying a product. You are buying a system. A way of doing things refined, tested, and handed from master to apprentice through wars, earthquakes, famines, depressions, and more.

Now let’s take a look at the American stock market. The Standard and Poor’s 500 (S&P 500) was created in March of 1957. Of the roughly 500 original companies, only 86 were still in the index 50 years later (1). The average tenure of a company in the index has fallen from 33 years in 1965 toward a forecast of roughly 14 to 15 years by the late 2020s (2).

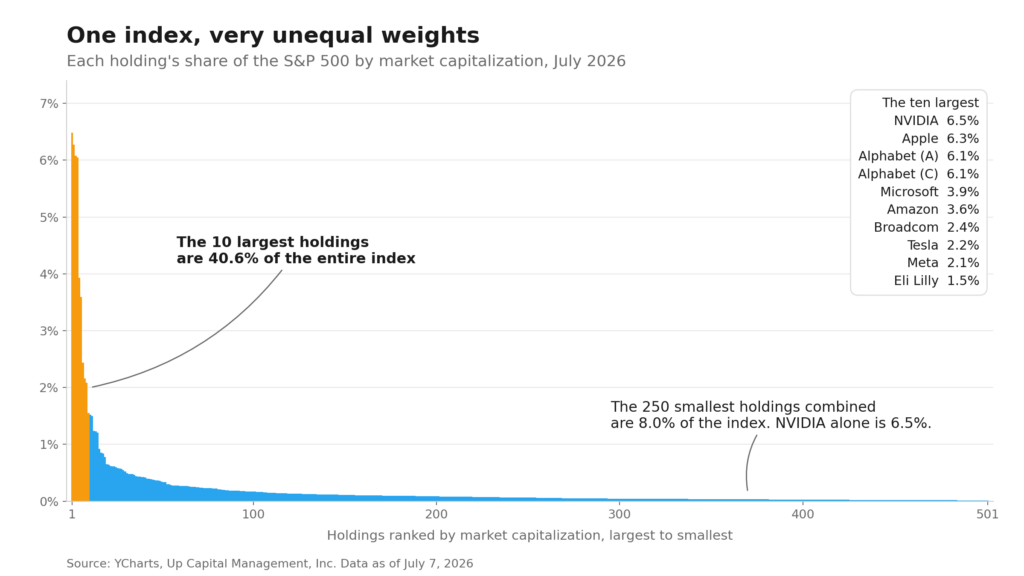

That raises the question everyone is asking right now, and one I heard a few times over the holiday weekend while socializing with friends, some working and some retired. Today, the ten largest companies make up roughly 40% of the S&P 500.

The chart above shows the concentration a lot of folks are worried about. Ten names recieving four of every ten dollars in the index. Is that unusual? Should it scare us?

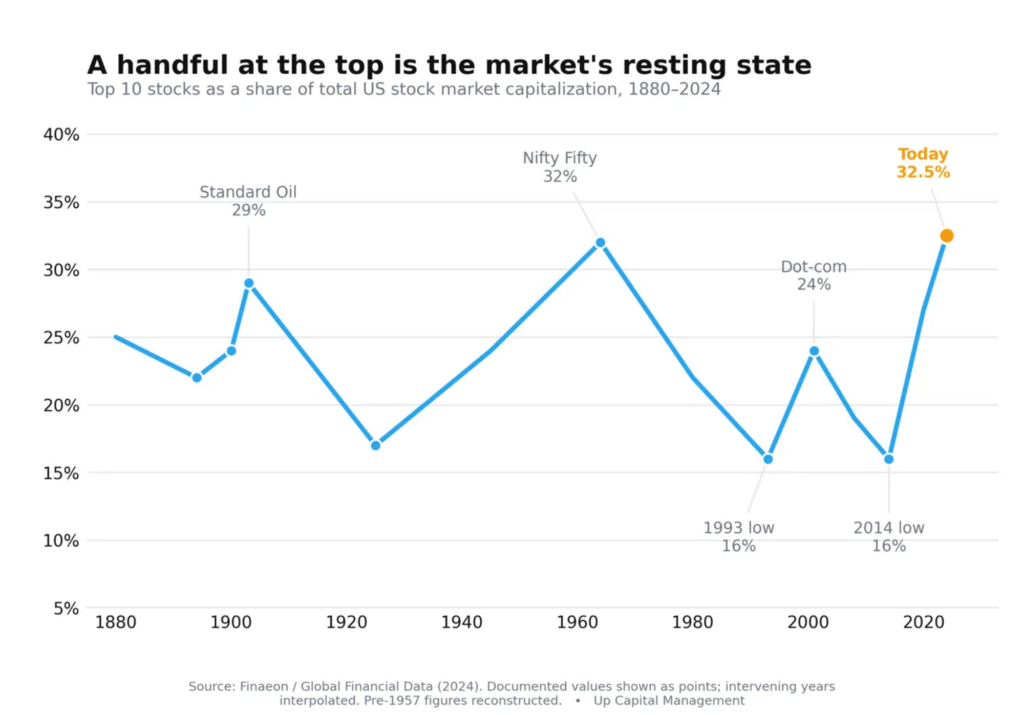

Here is what the long record shows. London Business School researchers Elroy Dimson, Paul Marsh, and Mike Staunton estimate the top ten stocks were about 38% of the American market in 1900, when Standard Oil alone was roughly 9%. In the mid-1960s, the era of IBM, General Electric, and Coca-Cola, the top ten again exceeded 40%. Concentration then fell for decades, bottoming near 16% in the early 1990s and again in 2014, before climbing back to today’s level (3).

This data runs through 2024 and spans the entire US market, but the takeaway stands. Today’s concentration is a level the market has reached before. A handful of dominant companies sitting atop the market kingdom is a resting state of the market and a feature of capitalism. What changes, relentlessly, is who holds the throne. Of the ten largest companies in the world in 2005, exactly one, Microsoft, still held its seat in the top ten in 2025.

Hendrik Bessembinder, a finance professor at Arizona State University, compounded the returns of every American stock since 1926 (this was before AI would take dozens of historical return streams and consolidate them for you in a click, God bless his heart). His finding is striking and lands its way into every meaningful conversation about investing for the long run. Roughly 4% of all companies account for the entire net wealth the U.S. stock market has created above Treasury bills, nearly six in ten stocks actually reduced shareholder wealth over their lifetimes, and just 72 companies produced half of all the wealth created for shareholders since 1926 (4).

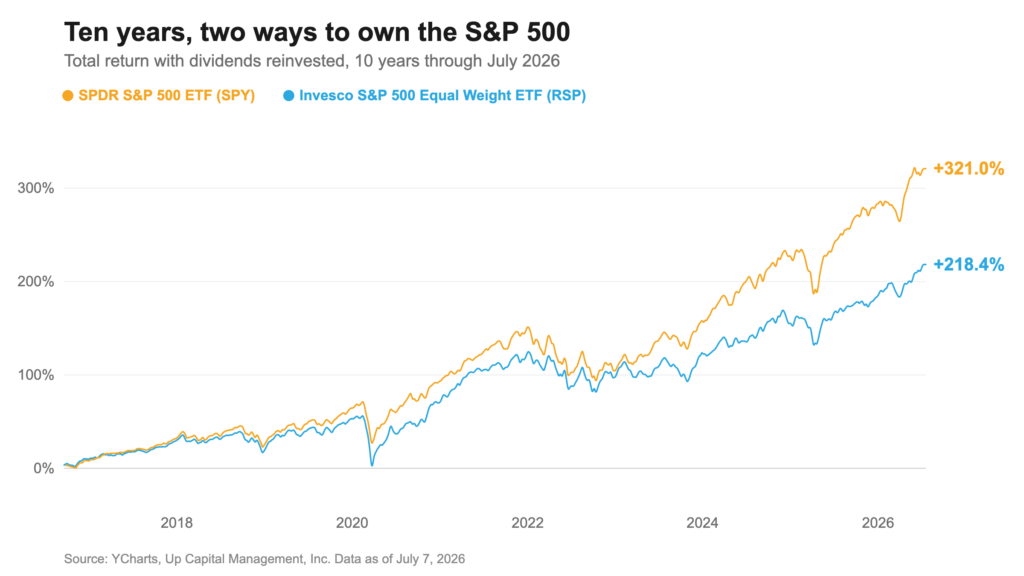

The 10-year chart above compares the S&P 500 (yellow), weighted by market cap, against an equal-weighted version (blue). The gap between the lines is the contribution of the giants, Bessembinder’s finding in real time. Returns are not spread evenly and are historically carried by a few.

The market’s great returns come from a small number of extraordinary, durable compounders, the closest thing we have to shinise. Economist Jeremy Siegel found something similar from the other direction. An investor who simply bought the original 1957 companies and held them, never chasing the new additions, outperformed the constantly updated index over the following 46 years. The single best performer was Philip Morris, a cash-generating consumer staple that turned $1,000 into roughly $4.6 million while the index turned it into about $125,000, which is still not bad (5).

I cannot tell you which of today’s giants will still lead the market in 2050. History says most will not, and history also says the market’s entire return will come from the few that do.

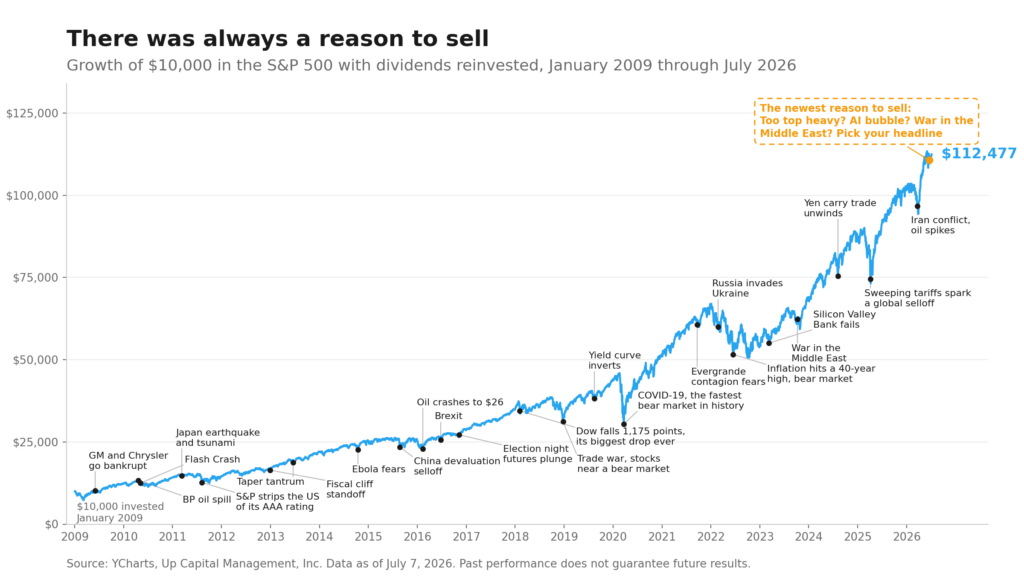

That resolves into one discipline which states that the reward goes to investors who own durable systems and hold them through everything. Every great compounder tested its owners brutally along the way. Nvidia, currently the largest company in the index, endured multiple declines of more than 50% on its climb to the top. The wealth went to the people who could stay in their seats, which is why the line often attributed to Warren Buffett rings true, “the stock market is a device for transferring money from the impatient to the patient.” Every dip on the chart below felt like the end of the world in the moment, but patience turned all of them into entry points in hindsight.

What does this mean to me?

Three things, practically.

You cannot consistently pick the ever rotating kings of the stock market kingdom in advance, so own them all. If 4% of companies create all the wealth, the surest way to hold the next generational compounder is broad, disciplined ownership of the market. That is why low-cost, diversified exposure sits at the core of every portfolio that we build for clients.

If you hold a concentrated winner, the question is not whether it is great. It is whether you can hold it through everything. Great companies fall 50% on the way to greatness. Position sizing, tax planning, and a written plan are what let you stay seated when it happens. Selling a winner in a panic and without a plan is how patient money becomes impatient money and gets transferred to the patient.

Judge your portfolio on a generational clock. The shinise measured success in centuries, not quarters. Your wealth plan should be built to outlive headlines, election cycles, and even you. The standard of durable systems, handed down with care, is what we hold ourselves to at Up Capital Management.

If you are holding a concentrated position and wondering how it fits into a long-term plan, or you simply want your portfolio stress-tested against history rather than headlines, that is exactly the conversation we are built for.

Sources

(1) Grobys, K. (2022). On survivor stocks in the S&P 500 stock index. Journal of Risk and Financial Management, 15(2), 95. https://doi.org/10.3390/jrfm15020095

(2) Innosight. (2021). 2021 corporate longevity forecast. https://www.innosight.com/insight/creative-destruction/

(3) Finaeon. (2024). 200 years of market concentration [Analysis using Global Financial Data series, 1875 to 2024]. https://finaeon.com/200-years-of-market-concentration/

(4) Bessembinder, H. (2023). Shareholder wealth enhancement, 1926 to 2022 (SSRN Working Paper No. 4448099). https://ssrn.com/abstract=4448099

(5) Siegel, J. J., & Schwartz, J. D. (2006). The long-term returns on the original S&P 500 firms (Working Paper No. 04-29). Rodney L. White Center for Financial Research, The Wharton School, University of Pennsylvania. https://rodneywhitecenter.wharton.upenn.edu/wp-content/uploads/2014/04/0429.pdf (Figures reflect February 28, 1957 to December 31, 2003.