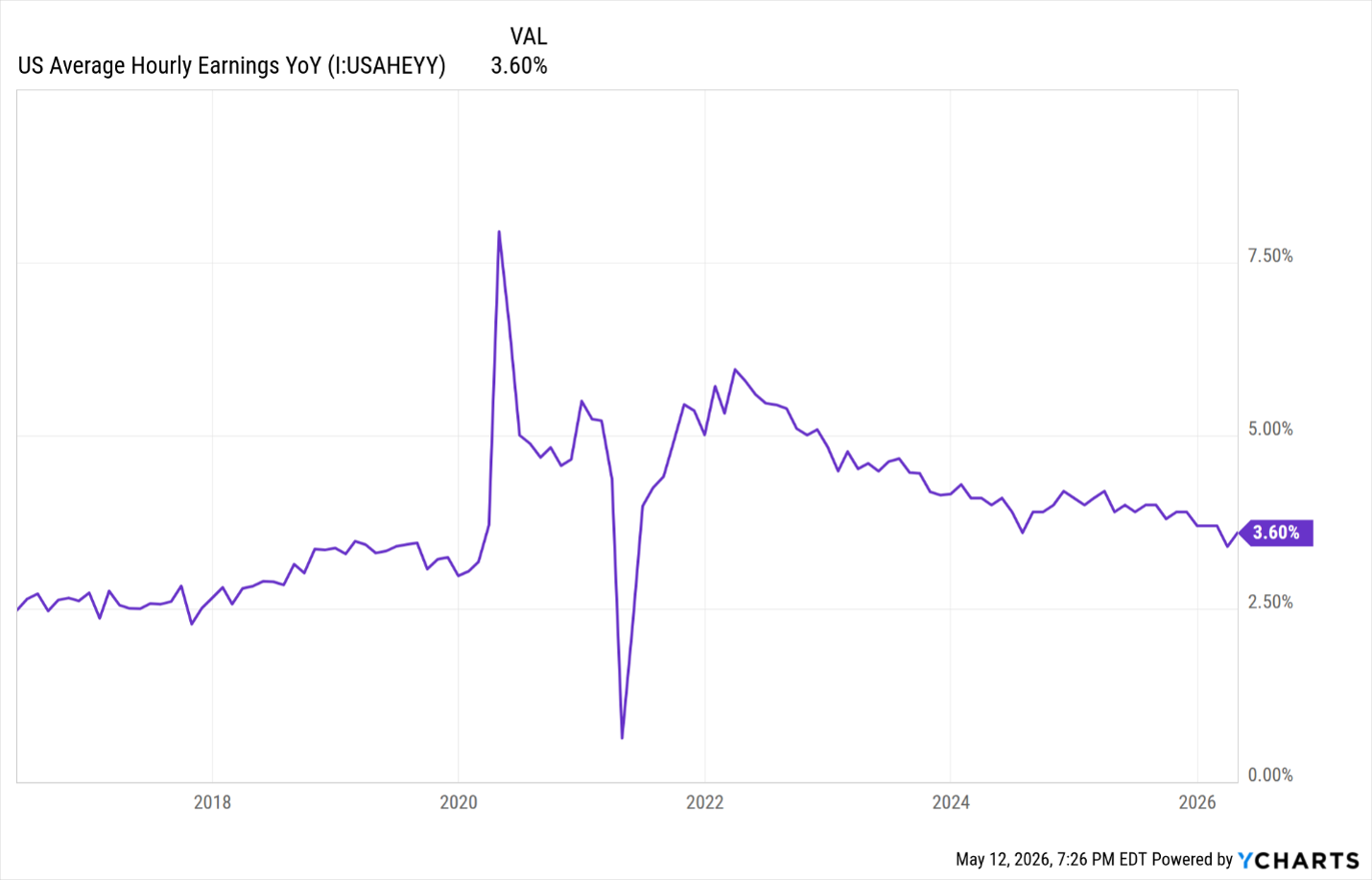

The US economy is still recovering from the significant whipsaw impact caused by the pandemic and related government restrictions on businesses and society. Last week, the Bureau of Labor Statistics reported that the year-over-year (YoY) increase in hourly earnings increased 3.6% from the same time in 2025 and is still ahead of rising costs. At the same time, unemployment has remained at historic lows for the past four years, with last week’s Unemployment rate at 4.3%.

For the past six years, the global shock of the pandemic has forced employers to make uneven adjustments to wages, particularly between essential and non-essential workers. Many restaurant owners I spoke with during the pandemic years continued paying base salaries during shutdowns to retain staff, even while their businesses were closed. In most cases, employees did return, but capacity limits reduced overall income, especially from tips. As restrictions eased, retail activity rebounded sharply. Eventually, businesses, particularly in retail, stabilized as consumer behavior gradually returned to more normal patterns.

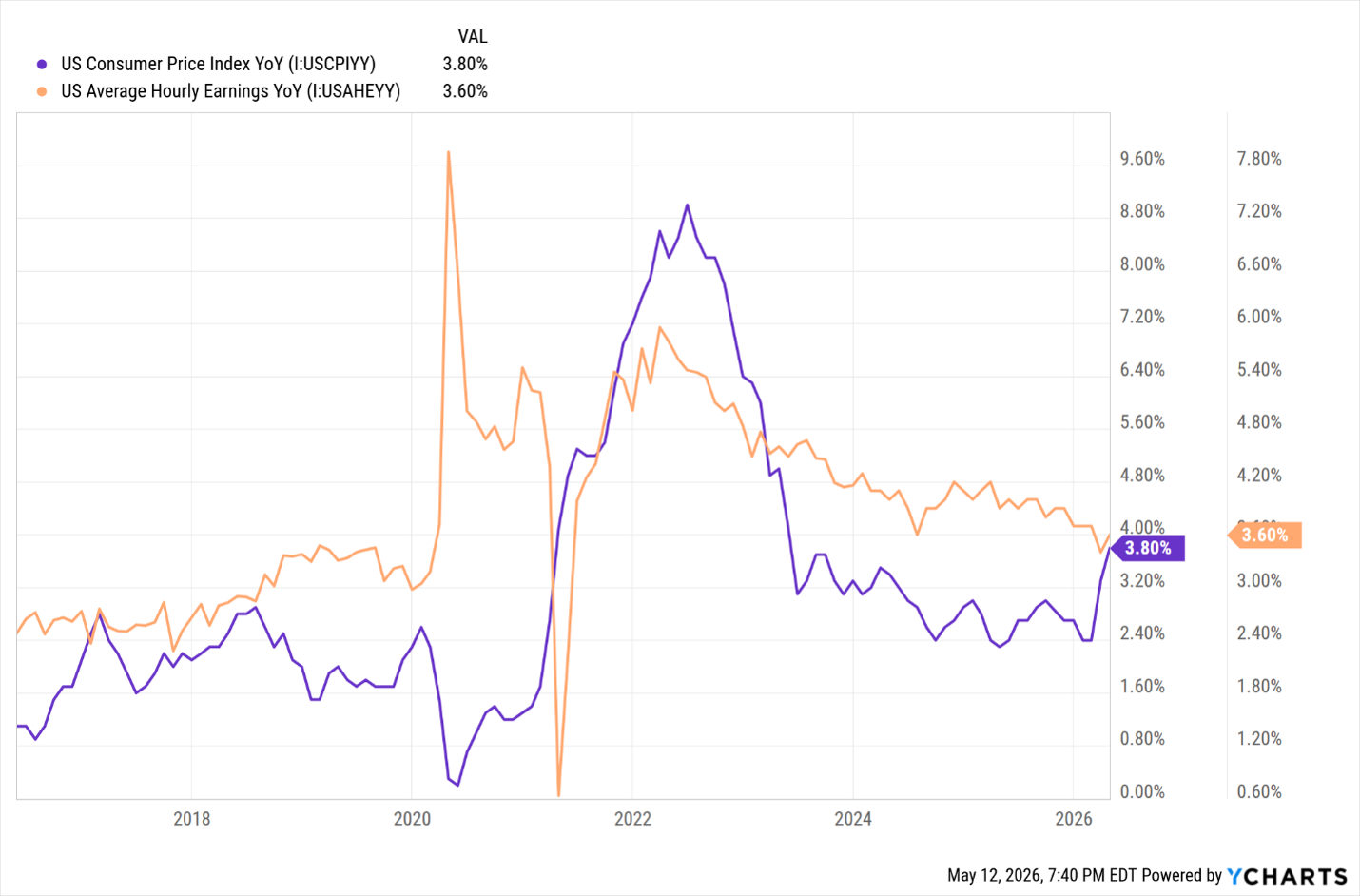

In the years leading up to the pandemic, wage growth consistently outpaced increases in the Consumer Price Index (CPI). That relationship reversed during the disruption of government-mandated closures and broader restrictions, pushing inflation ahead of wages. By 2023, however, inflation eased, and since then, wage growth has once again exceeded CPI increases.

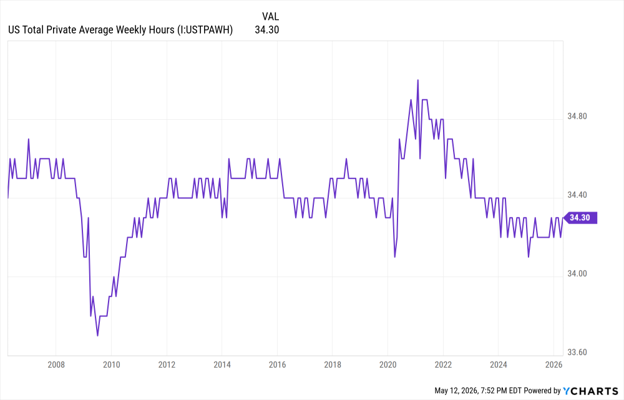

Ironically, even as the government shut down much of society, the average workweek soared to its highest level since 2000 as employers sent employees home to remote work. As the pandemic eased and restrictions were lifted, average weekly hours declined and now sit below pre-pandemic levels. This may be an early sign of the impact of AI on the labor market, with the decline of hours worked each week.

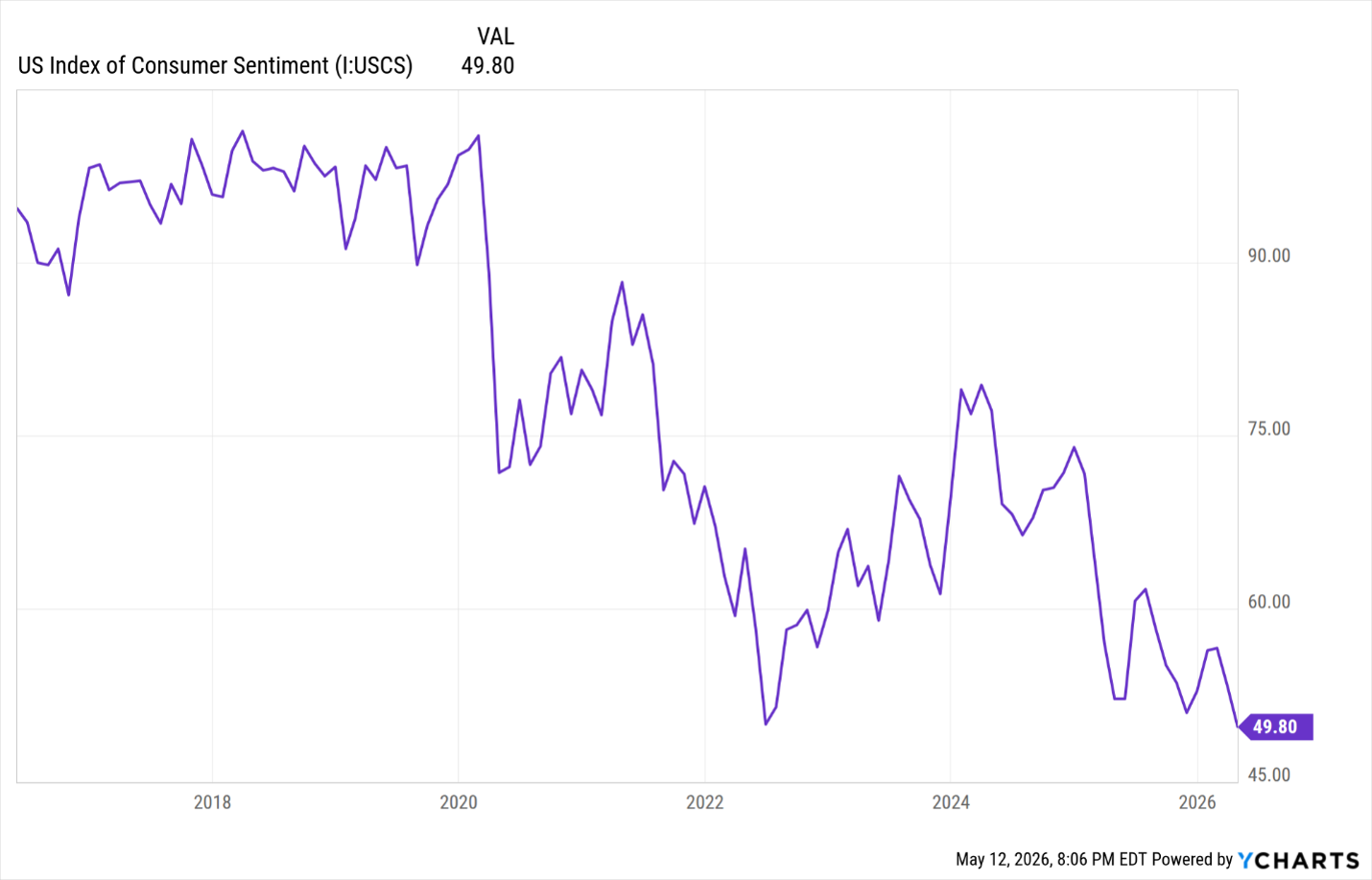

Understandably, these past six years have significantly impacted the emotional stability of individuals. Consumer Sentiment Index provided by the University of Michigan has whipsawed from near record highs prior to the pandemic to last month’s record low, surpassing even the lowest of depressed levels of consumer sentiment since the University of Michigan started reporting in 1972.

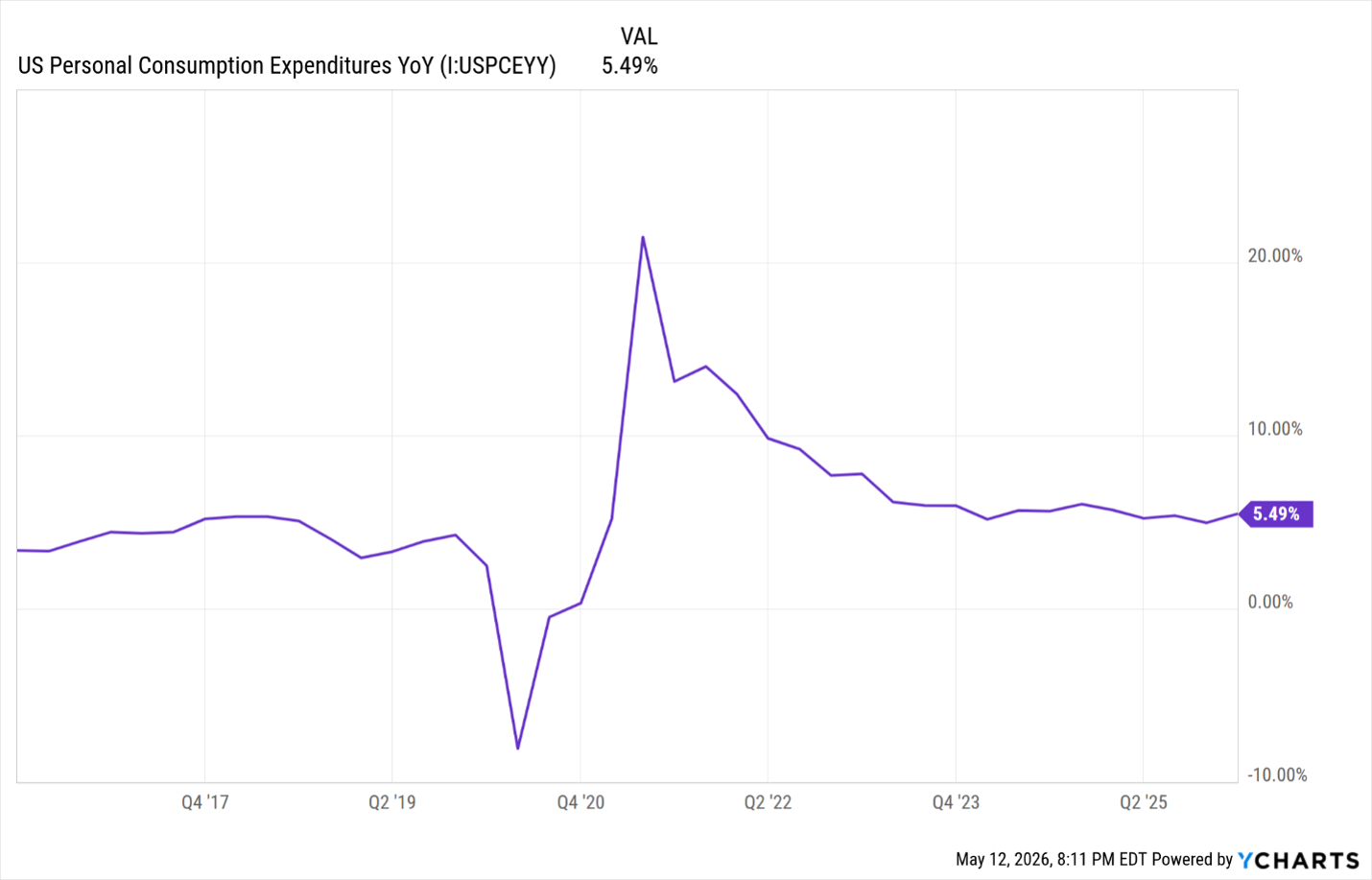

Through the various economic cycles since 2016, except for the sharp disruption during the early stages of the pandemic in 2020 and 2021, consumer spending has remained a primary driver of the U.S. economy. Recent year-over-year growth in Personal Consumption Expenditures (PCE) continues to run above pre-pandemic levels, underscoring the resilience of the American consumer and household incomes.

Consumer spending remains a critical pillar of economic growth and is one reason the U.S. stock market has largely looked past recent geopolitical tensions involving Iran and oil price volatility. Investors are focusing instead on continued US economic expansion and corporate earnings strength.

What Does This Mean to Me?

The health of US households and the strength of consumer spending are core components of the US economy. Consumer spending represents 66% of US commerce and is a key driver of economic growth. This is a unique aspect of the US economy compared to nearly all other countries that depend on government assistance and programs to fund their society.

We maintain our favorable view on the US economy and stock market. Give us a call if you have any questions about this UPdate or your own investment accounts. We welcome the opportunity to assist you and your family in achieving your goals.