In the past year, we have had several clients retiring from their professional careers. Most were clients for more than five years, and some for several decades. Back in 2019, nearly all of them asked the same question:“Can I retire in five years with our $1 million portfolio?”

Today, we’re hearing the same question from a new group of clients.

But the backdrop has changed. In 2019, the environment felt more supportive for investors. Multiple sectors were performing well, household incomes were rising faster than inflation, and net worths were growing, helped by strong 401(k) returns and appreciating home values. Looking ahead, many analysts expect the next five years to be more challenging than the last.

That shift has understandably created more uncertainty for those nearing retirement. For many, their current $1 million nest egg will be the foundation for meeting monthly income needs, especially for those planning to retire before Social Security begins. Just as important, that nest egg doesn’t stop working at retirement. It needs to continue growing, not only through the next five years, but for potentially 30 years or more beyond. An objective that many consider improbable.

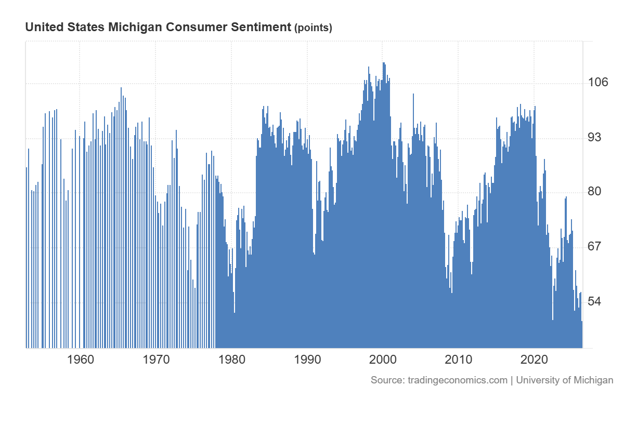

This may partially account for the 72-year record low of Consumer Sentiment as recently reported by the University of Michigan.

Preparing and staying retired requires focus on three key principles:

1. Building a financial plan with a high probability of success (90% or better)

2. Implementing disciplined and effective savings strategies

3. Managing portfolios for sustainable and reasonable returns now and throughout retirement

1. CREATING A FINANCIAL PLAN WITH 90+% PROBABILITY OF SUCCESS

The most important component of our Financial Plans is the probability analysis for our clients in achieving their financial goals throughout their lifetime. This is a complex calculation that factors client sources of income, spending needs, inflation, and historical investment returns through economic cycles of growth and contraction.

The income ledger includes all sources of retirement income that may include pensions (yes, some are still eligible for pensions), social security, rental property income, and distributions from retirement and non-retirement accounts. Expenses during retirement can still include children’s weddings, college expenses, and helping children buy a home. In addition, many of our clients like to budget during retirement for vacations (one or more per year), new cars every 5 – 7 years, healthcare needs, moving to new areas, and second homes. Each of these goals is modeled with its own expected rate of cost increases over time.

The preparation for your retirement is equally important. Paying down debts and mortgages reduces your income needs and taxes. Identifying what expenses will not be in your budget at retirement and determining what your net after-tax retirement income goal will be. Evaluating your post-retirement income opportunities. Many of our clients can work part-time or enter into consulting contracts with their current employer or others. Delaying or minimizing distributions from your investment accounts for income needs extends the appreciation period for your accounts.

The last component is determining a benchmark average return on all investments and year-end projected account values to achieve the retirement goals. We refer to this as the “glide path” to landing at retirement with the desired account balances and net worth. This is a critical aspect of the Financial Plan and one we refer to regularly to confirm our clients are on track to achieve their goals. However, the work does not stop at retirement. We continue to have annual updates and reviews of the Financial Plan after retirement to ensure they are on or ahead of the glide path to staying financially independent.

2. STRATEGIES FOR EFFECTIVE SAVINGS

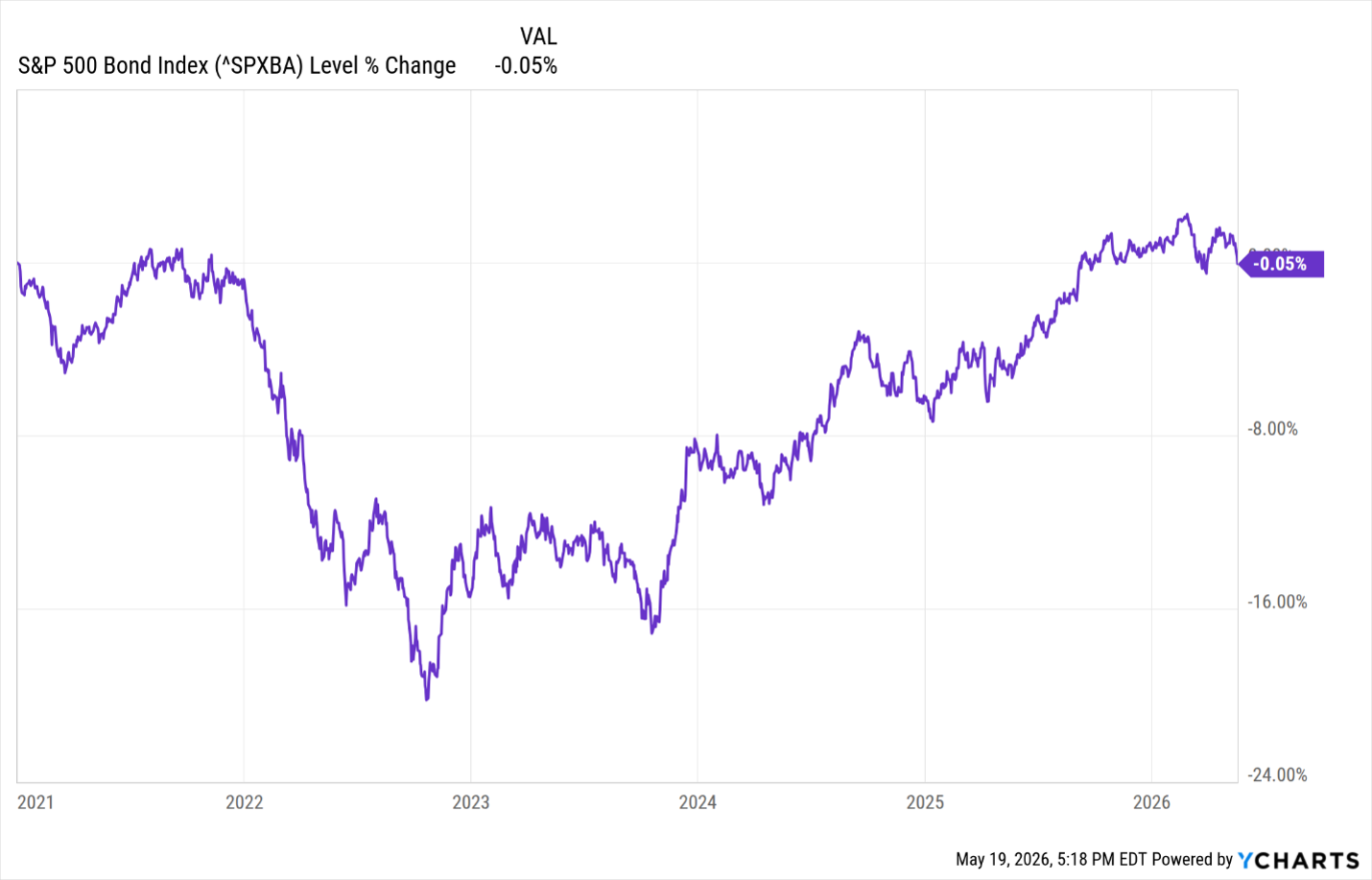

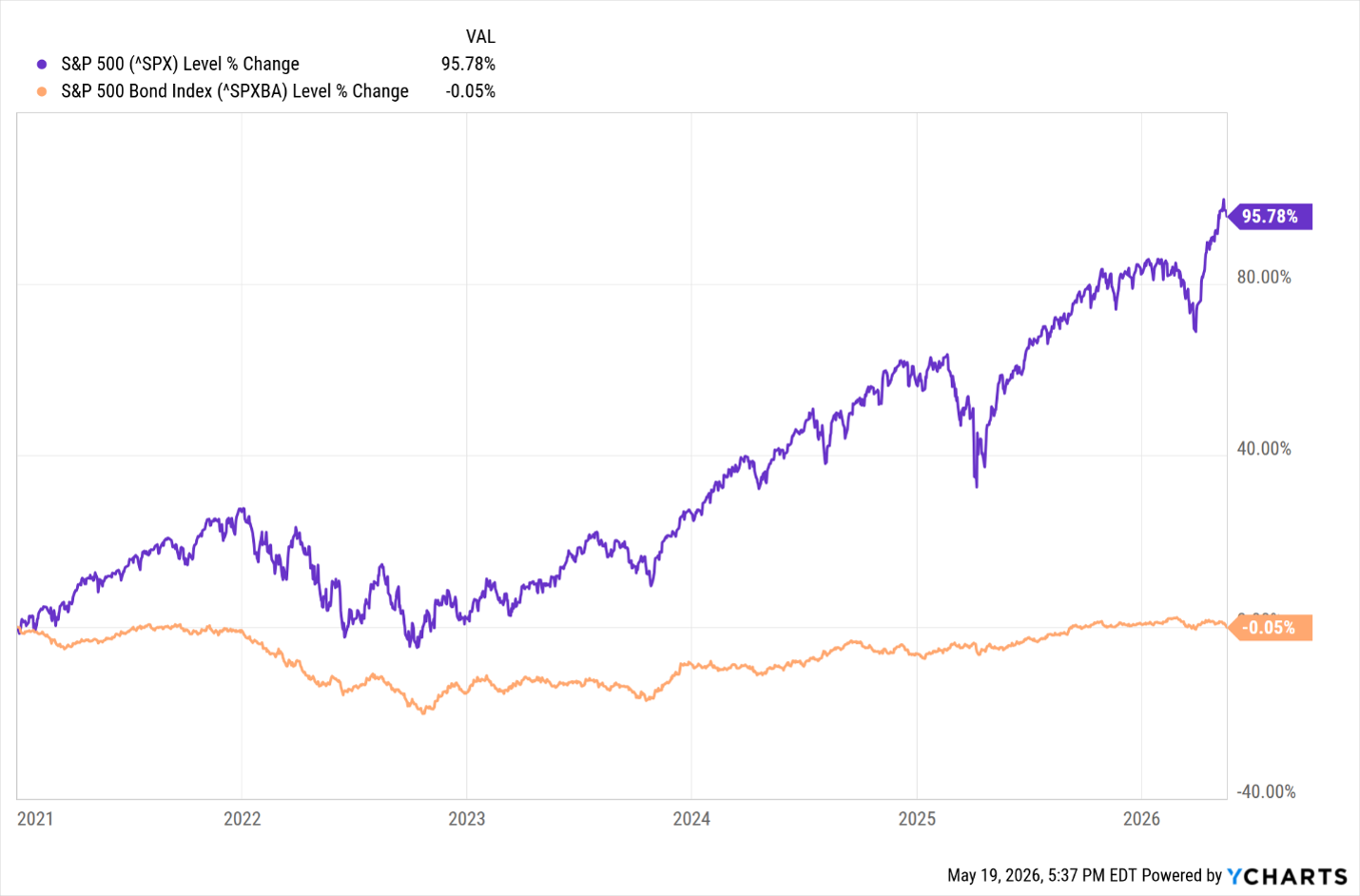

The most tax-efficient and convenient savings accounts are retirement plans, and especially those with employer matching contributions. Unfortunately, many of our clients are not completely aware of their retirement accounts regarding balances, employer matching, eligibility, and how their accounts are invested. It is typical for clients not to know their employer matching options, their own monthly contributions, or plan investing options. For many, their retirement plans are the largest and most tax-efficient asset to meet their retirement goals. Last year, we met with a couple (now a client) with little knowledge of how their retirement accounts were invested (401k, IRAs, and Roth). This was unfortunate as the plan administrator’s advisers are trained to adhere to traditional Modern Portfolio Theory that dictates reducing risk allocations as one approaches retirement age. Conservative investment funds are primarily invested in bonds and cash equivalents. For the past five years, the bond market has significantly underperformed the overall US stock market and, most importantly, has just recovered from the bond crash in 2022 – 2023. Since January 1, 2021, the S&P 500 Bond Index has had a cumulative return of -0.05%. You read that correctly, -0.05%.

As an example, let’s project that your current 401 (k) balance is $750,000, you contribute the annual maximum (currently $32,500) with an employer match of an additional $5000. The 401 (k) account invested in a bond fund based on the S&P 500 Bond Index for the past five years would have an estimated balance of $937,500. However, if the retirement account was invested in a fund with similar annualized returns to the S&P 500 since January 2021, the same savings and starting account balance would be approximately $1,737,054 in five years. An extra $800,000 can make a big difference going into retirement. See the chart below comparing the S&P 500 Stock Index to the S&P 500 Bond Index.

3. MANAGING PORTFOLIOS FOR SUSTAINABLE AND REASONABLE RETURNS

Managing portfolios for sustainable, reasonable returns requires discipline and consistency before and throughout retirement. The global economy is a complex, interconnected system, with countless forces influencing corporate growth and profitability. To stay ahead of these dynamics, we publish weekly observations on the economy and stock market.

Since 2020, investors have navigated an unusually volatile environment shaped by the pandemic, supply chain disruptions, inflation, rapid interest rate increases, a slower housing market, a commercial real estate crash, and ongoing geopolitical conflicts.

Looking ahead, many analysts expect the next five years to be more challenging than the last. Hopefully, that is an overstatement. Even amid recent uncertainty, the past five years have presented meaningful investment opportunities. Today, continued strength in AI and technology-related companies is creating new areas of growth and potential.

If history is any guide, volatility is not going away. Markets will continue to move through cycles of expansion and contraction. The key is staying focused on the fundamentals by monitoring economic indicators, recognizing emerging trends, and interpreting them within the context of historical patterns.

What Does This Mean to Me?

Building an estate that can support your financial needs indefinitely starts with a disciplined plan and consistent execution. Market conditions will continue to present challenges, so it’s important to identify the average rate of return your portfolio must achieve with retirement and non-retirement assets to meet your long-term goals.

In the years leading up to retirement, the objective is to lower that required return as much as possible. This can be done by reducing debt, increasing savings, and, when possible, achieving strong investment performance. Clients who reach a point where their goals no longer depend on earning a specific return have the highest probability of long-term success.

This is where we add value. We work with clients to clearly define their goals, develop thoughtful strategies, and implement them with discipline. Because not every strategy or investment performs as expected, we continuously monitor progress and adjust as needed.

If you’re interested in developing a comprehensive financial plan, we welcome the opportunity to speak with you.