Movement of Money

Businesses use fuel from the products they receive from manufacturing companies that feed the American engine. It's a symbiotic relationship of companies selling goods to their customers as manufacturers are producing and delivering more new products. The driver of the US economy is ultimately the demand from end users, whether business selling to business (B2B) or to consumers (B2C). The more transactions incurred with the buying and selling of goods increase the movement of money and the building blocks of the US economy.

A good sense of the health of the US economy is monitoring manufacturing activities that are at the beginning of the commerce cycle. Monitoring their production volume or inventory provides early signs of future trends of economic activity. Good indicators are rising manufacturing production, and concerning signs are slowing production or rising inventories, the result of production exceeding demand.

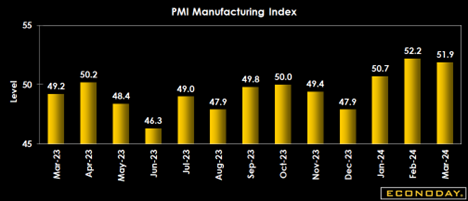

One economic indicator we watch is the US Purchaser Manufacturing Index (PMI). This index is based on monthly questionnaire surveys of selected companies that offer an advance indication of month-to-month activity in the private sector economy. This index tracks changes in variables such as production, new orders, stock levels, employment, and prices across manufacturing industries. Historically, when the PMI index is above 50, it represents a growing manufacturing industry, and below 50 indicates contraction.

Yesterday, IHS Markit released the monthly PMI report. Econoday offers this observation:

"PMI manufacturing ends March at 51.9, down a noticeable six tenths from the mid-month flash but confirming the third straight month above 50. February's reading for PMI manufacturing was 52.2, only slightly higher than March's final. The key to March's report is slowing growth in new orders, which was held down by a flat showing for foreign sales. Relying on back orders, the PMI sample increased the pace of production in the month; purchasing activity slowed, and inventories were drawn down. Hiring gains were modest, and price pressures for both inputs and selling prices rose."

On a global scale, the S&P Global Manufacturing PMI was revised lower to 51.9 in March 2024 from the preliminary 52.5 and compared to 52.2 final for February.

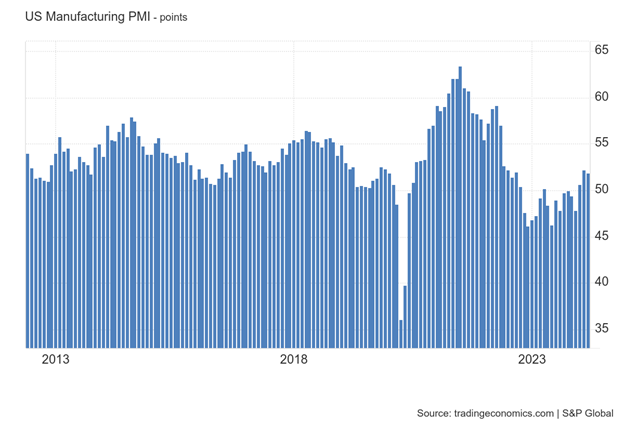

Trading Economics offered this observation of the March S&P Global PMI release:

"Signs of improving wider economic conditions and market demand fed through to a further expansion of US manufacturing production, with the rate of expansion hitting a 22-month high. The rate of job creation also quickened, but new order growth softened. Meanwhile, firms generally signaled a preference to draw down inventories amid sufficient holdings and efforts to improve cash flow. Purchasing activity and stocks of both inputs and finished goods were all scaled back following increases in February. On the inflation front, sharper rises in both input costs and output prices were registered. Also, firms remained confident that output will increase over the coming year, thanks to expectations for improving economic conditions, marketing efforts, and improving capacity."

The rebound, both domestically and internationally, in manufacturing seems to be continuing after the significant whipsaw of production from the pandemic. Businesses were shut down, and employees were sent home in 2020, which collapsed economies all around the world. Many countries maintained draconian policies for years, forcing citizens to remain at home and devastating their economies. China held its inconceivable zero-tolerance policies for years following the outbreak. It was only on December 8, 2022, that the Chinese government issued new guidelines allowing people to leave their homes for the first time since early 2020, reversing their strict zero-tolerance COVID policies.

As experienced in dramatic fashion in 2020, when consumers and businesses slow or stop buying, the manufacturing industry responds accordingly. Early signs of the slowing of the economic engine or potentially a recession are when buying and selling slows the movement of money declines.

Both the US and Global PMI have been steadily improving since bottoming in late 2022, and both are above a 50 reading, indicating growth in this sector. Positive indicators in the manufacturing sector are encouraging indicators that money will continue to circulate around the economy for economic growth in the US and around the world.

What Does This Mean to Me?

The US stock market finished the first quarter with strong results, while the bond market struggled with rising interest rates. The small cap index continues to lag behind. Below are the major indices YTD performance through March 31, 2024:

S&P 500: 10.16%

DJIA: 5.62%

NASDAQ: 9.11%

S&P 400 (Mid Cap): 9.52%

S&P 600 (Small Cap): 2.00%

S&P Bond Index: - 0.49%

We would anticipate a short-term weakness in the stock market after a strong first quarter. Investors seem to believe that for the US economy to continue its positive trend, the Federal Reserve needs to reduce interest rates. We question the narrowness of this focus as the complex networking of domestic and global economies is not dependent on singularly interest rates and credit markets. I listened to and spoke with many financial professionals with global experience at the conference I attended in Denver last week. Most agreed the US was currently the best-performing country of the G-7 nations and most other countries, large and small. A strong US economy will continue to be the recipient of foreign investment and strong trading partnerships for our domestic companies. The labor market remains strong with more people working in the history of this country. Finally, both consumer and business spending and confidence remain positive for the near future. We maintain a favorable view of the US stock market and economy.

Therefore, at this time, we would view market weakness as a buying opportunity. Let us know your thoughts on this Weekly Brief. More importantly, give us a call to schedule a time we can meet to discuss ways we can assist you and your family in achieving your financial goals.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions