Factors Orders are Rising

On Monday, the Bureau of the Census, U.S. Department of Commerce. Released its monthly U.S. Factory Orders report. New orders for U.S. manufactured goods fell 1.6% month-over-month (MoM) in January after a 1.7% rise in December. This decline for January was less than forecast. However, unpacking the report, there is a lot of encouragement for the start of the year for the economy.

Excluding commercial aircraft, which declined 54.5% in January after a 105.6% jump in December and Transportation, Factory Orders increased by 1.2% or double analysts' forecast of a 0.6% gain.

Econoday provided this commentary on the report:

“But the verdict isn't flat at all. A big positive that makes January a strong month is core capital goods orders (nondefense aircraft). These jumped an outsized 0.8 percent, getting business investment off to a great first-quarter start. Keys here are a 7.0 percent surge in computers and related products and a 1.6 percent jump in machinery orders led by industrial machinery.

Orders for nondurable goods, which are always sensitive to monthly swings in petroleum-based products, rose 1.5 percent following declines of 1.7 and 2.1 percent in the two prior months. Orders for durable goods are unrevised at last week's initial decline of 4.5 percent.

Other details to note include a 54.5 percent swing lower for commercial aircraft following December's 105.6 percent jump and a 1.4 percent rise for motor vehicle bodies, parts, and trailers that follows a 0.7 percent December decline. January's rise for the latter offers further evidence of new supply underway for the auto industry. Total shipments rose 0.7 percent in January, total unfilled orders, as well as total inventories, were unchanged.”

The stock market started the year with a strong rally after the 2022 selloff that dipped into correction territory several times throughout the year.

NASDAQ sold off sharply in 2022 with a 32% decline, and typical for the market, NASDAQ had one of the strongest bounce-backs in January.

Solid economic news like the January Factory Orders report will be key for the U.S. economy and stock market to continue its positive trend.

Germany also released its Factory Orders report yesterday. Germany's economy has been impacted by the Ukraine war and soaring energy prices. The Factory Orders in Germany increased that was 1% in January MoM following December's 3.4% increase.

Trading Economics had this commentary on the report:

“Foreign orders led the gains (5.5%), with those from countries outside the Euro Area surging 11.2%, mainly boosted by aircraft and spacecraft construction. On the other hand, orders from the Euro Area decreased by 2.9%, and domestic orders sank by 5.3%. Meanwhile, orders went up for capital goods (8.9%), namely aircraft and spacecraft construction (138.5%) and manufacture of motor vehicle engines (6.8%). On the other hand, orders contracted for intermediate goods (-8.9%) and consumer goods (-5.5%), namely electrical equipment manufacturing (-22.3%). Excluding large-scale orders, factory demand went up 2.9%” source: Federal Statistical Office

U.S. investors can become complacent with the stability of the American economy. Germany is the economic engine of the European Union that has to lead the union with fiscal and monetary policies. Notice the volatility of the German Factory Orders report, with most of the increase from outside the Euro Area, and more disturbing is the significant decline of consumer goods (-5.5%) and electrical equipment manufacturing (-22.3%).

Unlike the U.S., consumer spending only represents 41% of Germany's GDP vs. the U.S. of 66%. Nonetheless, consumer spending is key for both countries, and the good news for the U.S. is consumer spending increased in January vs. Germany's decline.

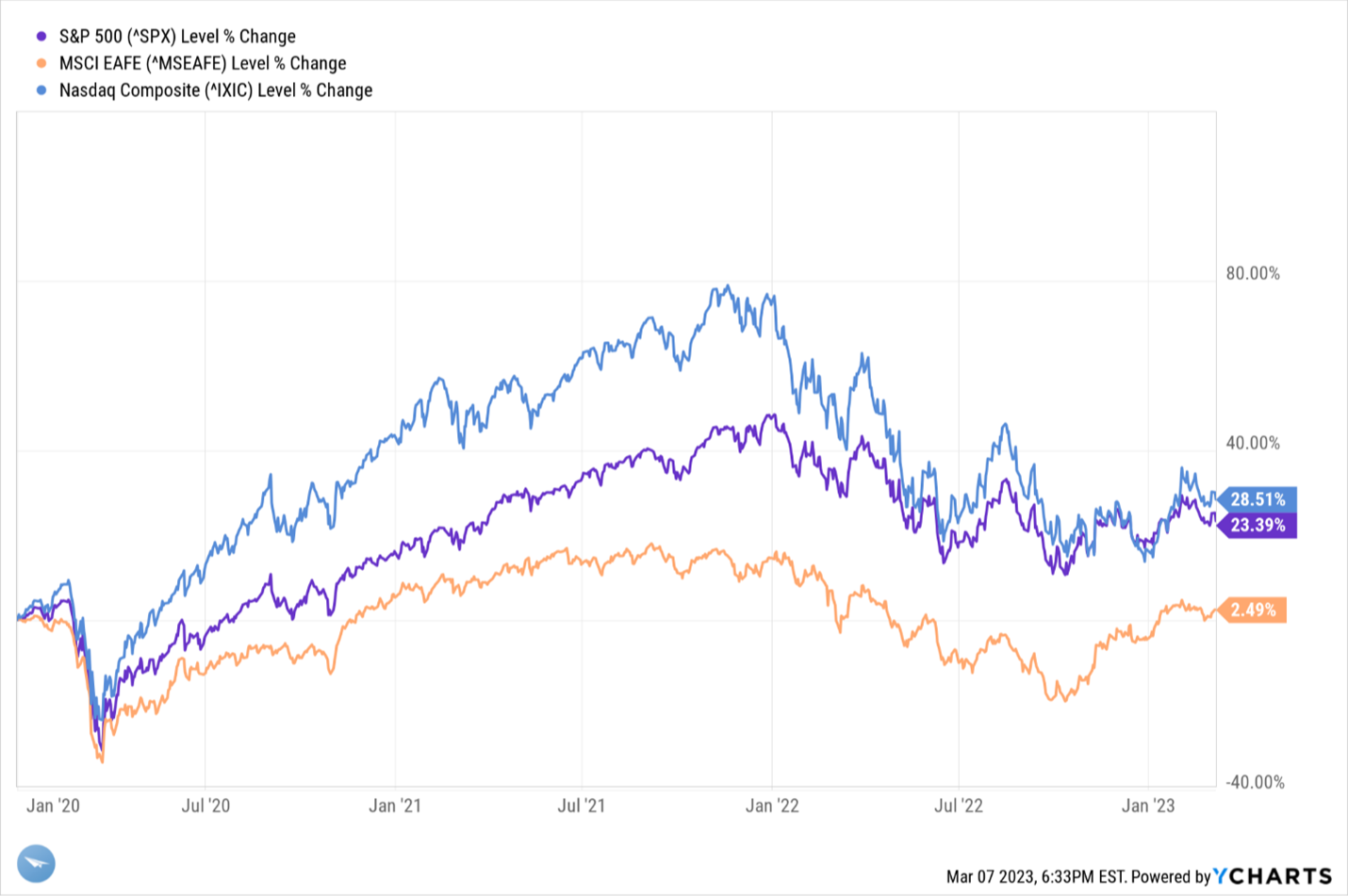

Also, notice the percentage fluctuations for the past three years. At first, the two charts above look similar until you notice that the chart for Germany's right-side percentage tables is double the range compared to the U.S. While the U.S. experienced 2020 as much as 8% MoM decline, Germany experienced almost 23% decline. The more stable and consistent U.S. recovery has resulted in a stronger stock market rally. Since the pandemic, the S&P 500 has trounced the MSCI EAFE index with a 23.39% gain vs. 2.49%, respectively, since January 1, 2020. NASDAQ, the stronger performer through 2021, gave up most of its lead over the S&P 500 in the 2022 selloff.

What Does This Mean to Me?

The U.S. economy continues to show moderate gains from the pandemic. However, investors are in a state of panic about anything that may indicate the Federal Reserve will raise the discount rates past their 5.25% – 5.5% target. Unfortunately, the good news of economic growth is bad news as it may indicate that inflation is not settling down fast enough for Jerome Powell and his Federal Open Market Committee (FOMC). Investors still fear the Federal Reserve will drive the U.S. economy into a recession despite the seemingly controlled slowing of inflation with rising interest rates without much collateral economic damage.

Referring to technical indicators, it is positive that the S&P 500 rallied in January above its previous high reached on December 1, and the February pullback did not drop the index below the previous low reached on December 30. Also, the index remains above its 200-Day Moving Average (DMA) and within 0.5% of both its 20 DMA and 50 DMA. The upward trend remains in tack.

NASDAQ also remains in a positive trend with the same technical indicators as the S&P 500.

Although we maintain our favorable rating on the U.S. economy and stock market, our expectations for the yearly gains for the S&P 500 and NASDAQ remain modest. We anticipate gains in the 7% – 10% range for the S&P 500 and 9% – 15% for NASDAQ. Both indices achieved these annual gains in January and have since pulled back 37% and 56%, respectively. We would anticipate both indices and the stock market to have the year of two steps forward and one back. January was the two steps forward, and February was the one step back. Not a bad trend for investors except those that expect 1% daily gains and 20% annual returns.

Give us a call if you have any questions about this Weekly Brief or your investing and financial planning. We welcome the opportunity to be of service.

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. Some of this material was developed and produced by FMG Suite to provide information on a topic that may be of interest. FMG Suite is not affiliated with the named representative, broker - dealer, state - or SEC - registered investment advisory firm. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions