Weekly BriefFebruary 11, 2026•7 min read

Over the past three days, we’ve received reports on the state of consumer sentiment and small business confidence. The results show that both groups are slowly becoming more optimistic about the future, though improvement remains modest.

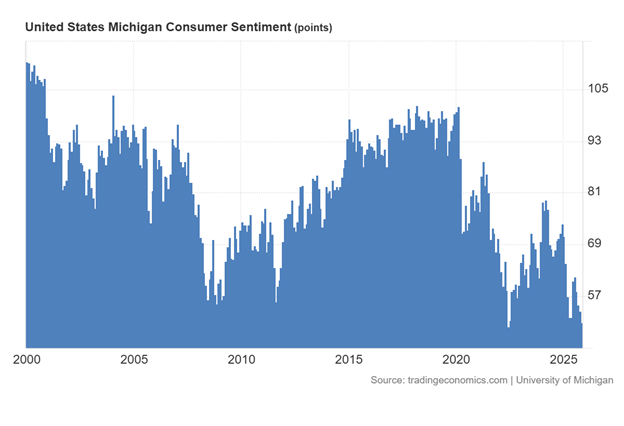

Starting with consumers, the University of Michigan’s monthly sentiment report, released Friday, showed only a slight uptick. Sentiment rose by 0.9 points in January to 57.3 and is still far below the long-term benchmark of 80, which typically reflects a moderately positive outlook.

As the chart below illustrates, consumer sentiment peaked in 2000 before entering an eleven-year period of steady decline. Sentiment eventually bottomed out in August 2011 as the effects of the Great Recession gradually eased. From that point, optimism improved as economic conditions strengthened, job growth accelerated, and equity markets rallied.

Sentiment reached a near all-time high of 101 in February 2020, but that surge was abruptly reversed by the onset of the global COVID-19 pandemic. A brief recovery in 2021 and early 2022 was again derailed when inflation climbed to levels not seen since 1979, prompting the Federal Reserve to launch an aggressive interest-rate hiking cycle.

Consumer sentiment fell to its lowest level since 1972 as mortgage rates surged, pricing millions of prospective homebuyers out of the housing market.

Sentiment began recovering in 2023, with consumers’ views of their personal finances and the broader economy improving steadily. Optimism reached a high of 79.5 in March 2024. However, since then, sentiment has weakened again as concerns over tariffs, persistently high costs, and uncertainty surrounding President Trump’s new policies have dominated the outlook.

In this month’s report, the Consumers Director, Joanne Hsu, provided this commentary,

“Consumer sentiment was essentially unchanged, inching up less than one index point from last month and sitting about 20% below January 2025. Sentiment surged for consumers with the largest stock portfolios, while it stagnated and remained at dismal levels for consumers without stock holdings. On net, modest increases in current personal finances and buying conditions for durables were offset by a small decline in long-run business conditions. While sentiment is currently the highest since August 2025, recent monthly increases have been small—well under the margin of error—and the overall level of sentiment remains very low from a historical perspective. Concerns about the erosion of personal finances from high prices and elevated risk of job loss continue to be widespread.”

Even with the strong U.S. stock market rally since January 2023, consumers report only a modest improvement in their personal financial conditions. Investors with 401(k) accounts allocated to the S&P 500 or growth-oriented funds have seen balances rise more than 80% over that period. Yet, it appears that even a near doubling of retirement savings over three years has not been enough to significantly boost consumer confidence.

Today, the official release of retail holiday sales confirmed what many feared. Dire consumer sentiment leading up to the holidays did indeed influence their spending. Instead of a year-over-year (YOY) increase last December, sales had barely increased. According to theUS Census Bureau, 2025 holiday retail sales increased a mere 0.6% YOY. In today’s report, the US Bureau stated the following:

“Advance estimates of U.S. retail and food services sales for December 2025, adjusted for seasonal variation and holiday and trading-day differences, but not for price changes, were $735.0 billion, virtually unchanged (±0.4 percent)* from the previous month, and up 2.4 percent (±0.5 percent) from December 2024. Total sales for the 12 months of 2025 were up 3.7 percent (±0.4 percent) from 2024. Total sales for the October 2025 through December 2025 period were up 3.0 percent (±0.4 percent) from the same period a year ago. October 2025 to November 2025 percent change was unrevised from up 0.6 (±0.3 percent). Retail trade sales were virtually unchanged (±0.5 percent)* from November 2025, and up 2.1 percent (±0.5 percent) from last year. Nonstore retailers were up 5.3 percent (±1.4 percent) from last year, while food service and drinking places were up 4.7 percent (±1.8 percent) from December 2024.”

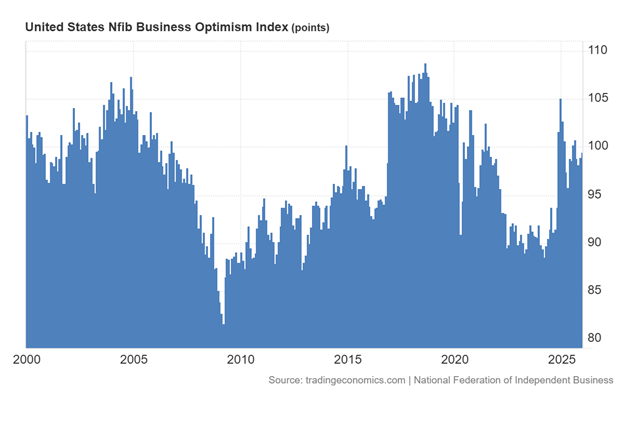

Small business owners, meanwhile, appear to be growing more upbeat. Since 2000, small business sentiments have followed a cycle similar to that of consumer confidence. However, after bottoming in March 2024, optimism among small business owners has improved significantly.

By December 2024, the National Federation of Independent Business (NFIB) sentiment index surged to 105.1, its highest level since 2020. Historically, readings above 100 signal solid optimism among small business owners.

In January, the index slipped slightly to 99.3, but it remains within a range that suggests generally positive sentiment and continued confidence in the outlook.

The NFIB cited the following key findings in this month’s survey:

In January, 13% reported the cost or availability of insurance as their single most important problem, up 4 points from December. The last time insurance reached this percentage was December 2018.

Sixty percent of small business owners reported capital outlays in the last six months, up 4 points from December and the highest level since November 2023.

In January, a net negative 6% of owners reported paying a higher interest rate on their most recent loan, down 3 points from December. This suggests that credit markets are turning more favorable for small borrowers.

In January, 16% of small business owners cited labor quality as their single most important problem, down 3 points from December. This is the third consecutive month that labor quality has been reported as the single most important problem, and it has declined.

The net percent of owners expecting higher real sales volumes over the next quarter rose 6 points from December to a net 16% (seasonally adjusted).

The net percent of owners reporting inventory gains rose 4 points to a net 3% (seasonally adjusted), the highest reading since January 2023. Not seasonally adjusted, 14% reported increases in stocks (up 1 point), and 17% reported reductions (up 2 points).

In January, 62% of small business owners reported that supply chain disruptions were affecting their business to some degree, down 2 points from December. Four percent reported a significant impact (up 1 point), 17% reported a moderate impact (down 4 points), 41% reported a mild impact (up 1 point), and 37% reported no impact (up 2 points).

The net percent of owners raising average selling prices fell 4 points from December to a net 26% (seasonally adjusted). Price increases remain well above the historical average of a net 13%, suggesting continued inflationary pressure. Looking forward to the next three months, a net 32% (seasonally adjusted) plan to increase prices, up 4 points from December.

In January, overall reported business health improved from December, with more reporting it as excellent and fewer reporting it as fair. When asked to evaluate the overall health of their business, 14% rated it as excellent (up 5 points), 54% rated it as good (unchanged), 27% rated it as fair (down 7 points), and 4% rated it as poor (up 1 point).

Overall, business owner sentiment is solid and indicates optimism for the future of their businesses. Based on the survey, business owners expect to raise prices. If so, inflation may become an issue for the Federal Reserve and consumers.

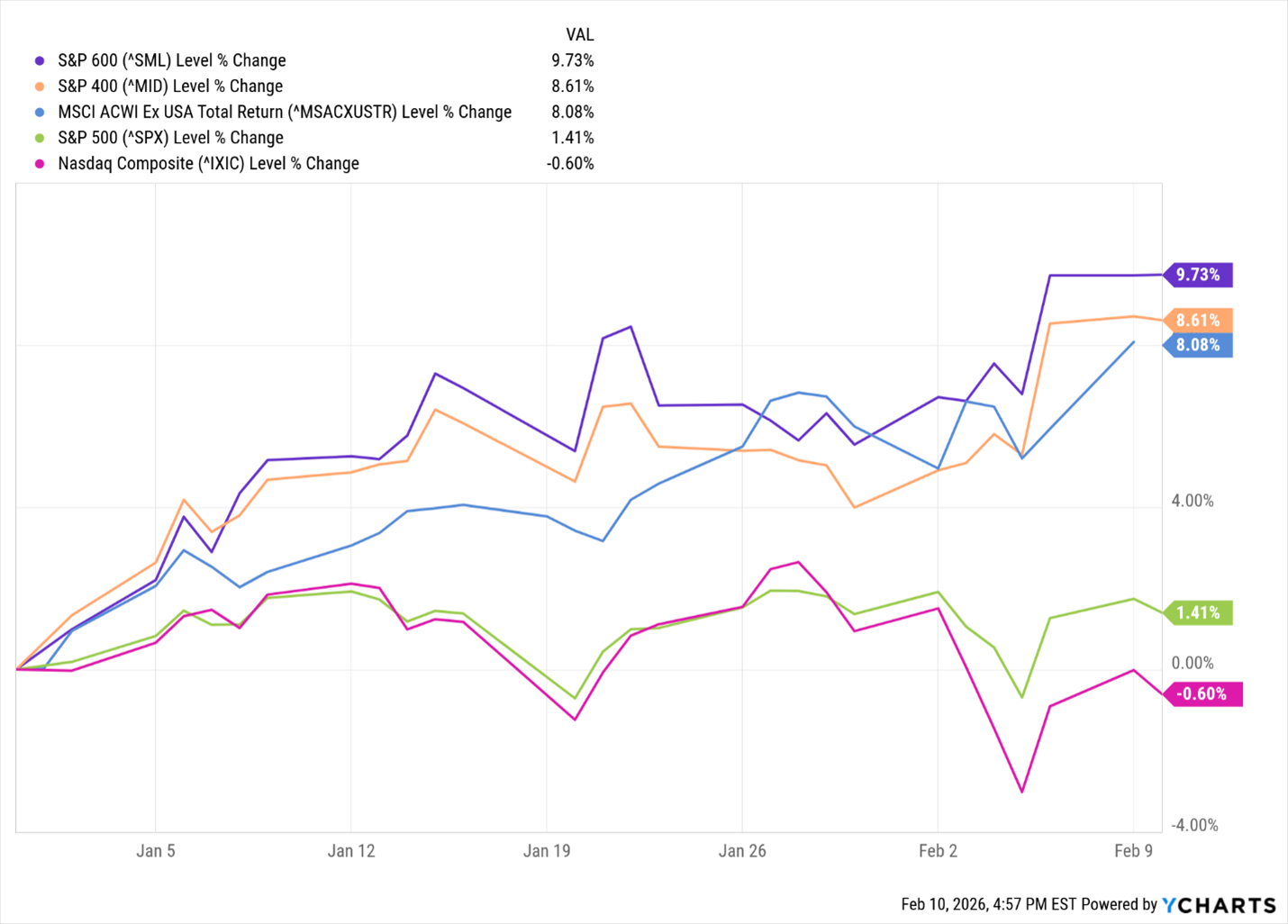

Since the S&P 500 and NASDAQ peaked on October 28, 2025, the market’s former laggards have emerged as the new leaders. The MSCI Ex-U.S. Index outperformed the major U.S. indices throughout 2025 and has continued to lead on a year-to-date basis.

In addition, the S&P 400 MidCap and S&P 600 SmallCap indices have moved ahead of large-cap stocks since September 2025. So far this year, the index performance leaderboard has largely flipped compared with 2025, aside from continued strength in international equities.

Mid- and small-cap indices are now well ahead of the S&P 500 and NASDAQ, marking a notable shift in market leadership.

Given improving small business sentiment and the recent rally in small and mid-cap indices, it may be an appropriate time to begin adding modest allocations to these sectors. That said, caution is warranted. Historically, rallies in smaller-cap stocks have often faded quickly in response to factors such as slowing economic momentum, rising interest rates, persistent inflation, and higher input costs.

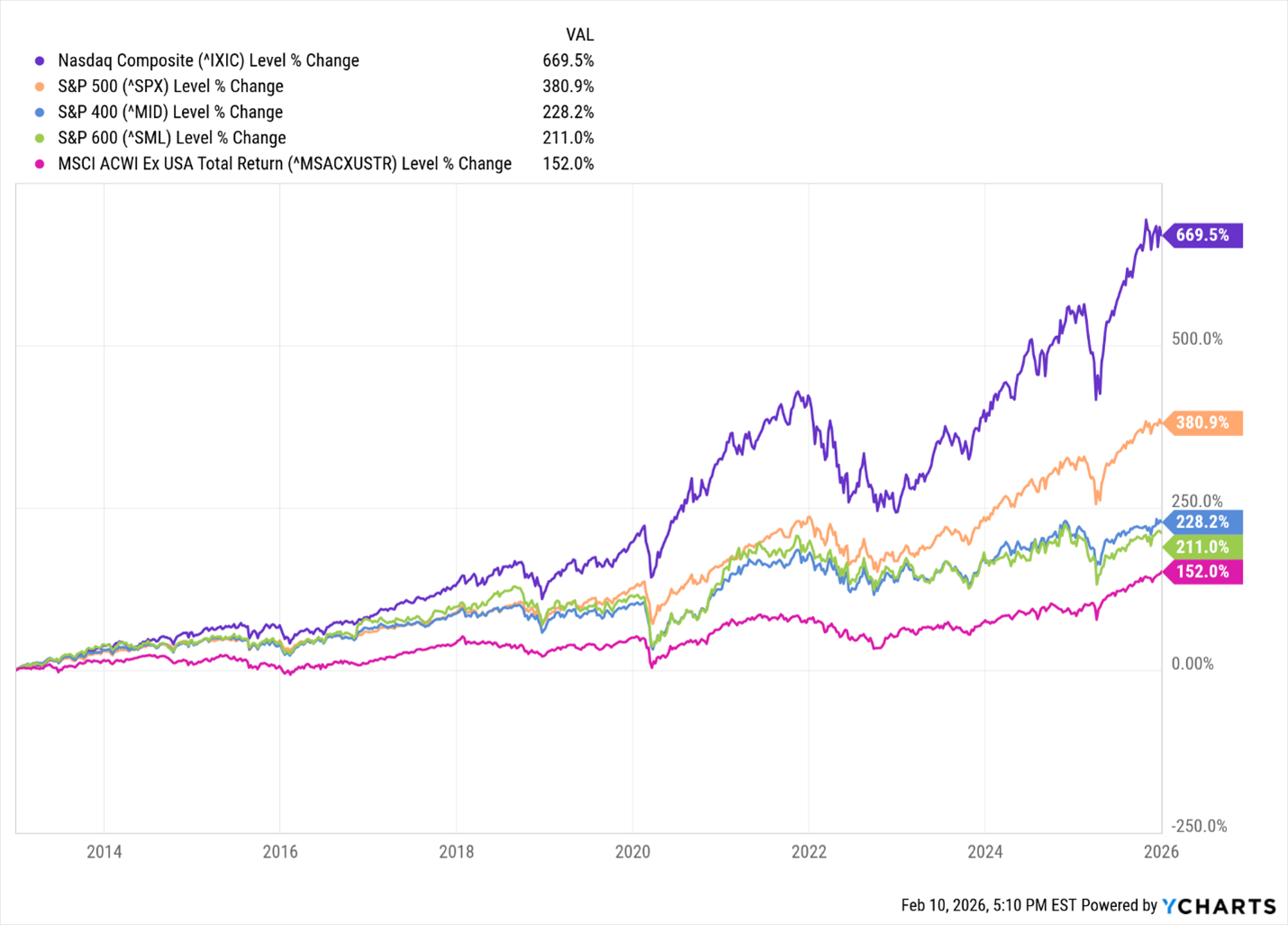

Even so, small- and mid-cap indices have significantly underperformed the S&P 500 and NASDAQ since 2013 by roughly 50% and 65%, respectively. This prolonged lag suggests that a period of mean reversion may be approaching, making a measured re-entry into these segments increasingly compelling.

We maintain our favorable view of the US economy and stock market. We anticipate this year for more surprises from Washington and similar stock market fluctuations. However, we also believe the year will end positively for the stock market. Patience, we believe, will be rewarded.

Anton Bayer

Back to Blog