BLOG

Signals of a Stock Market Crash

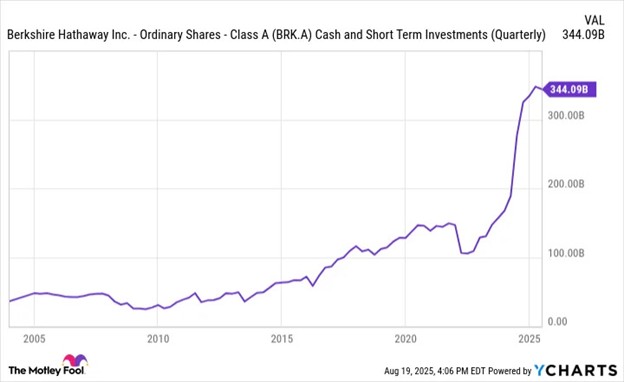

Investors are enjoying a robust stock market rally with NASDAQ and possibly the S&P 500 completing three consecutive years of 20%+ annual gains. Meanwhile, Berkshire Hathaway has amassed a record-breaking cash reserve, reaching an all-time high of $347.7 billion in the first quarter of 2025. This represents more than a threefold increase in just three years, driven largely by aggressive stock sales and what their investment committee perceives as a lack of attractive investment opportunities.

Warren Buffett, CEO of Berkshire Hathaway, is well-known for building large cash positions when he believes markets are overvalued—often years in advance of a downturn. In mid-2005, Berkshire raised its cash reserves to what was then a record $48 billion, three years before the 2008 financial crisis.

Buffett followed a similar approach during the 1990s, choosing caution over hype during the dot-com boom. He steadily grew Berkshire's cash reserves throughout the decade, notably in 1993 and again in 1999, as tech stocks soared. Between 1992 and 1999, the NASDAQ surged 594%, averaging 31.4% annual growth. While Buffett missed much of that rally, his caution proved wise when the bubble burst in 2000, sending tech stocks tumbling and many dot-com companies into bankruptcy. Below is a chart of Berkshire’s cash reserves in dollars compared to the NASDAQ index. Note the significant decline in cash reserves, although still high, months before the beginning of the 2000 Dot-com bust.

Buffett’s instincts about market overvaluation are rarely wrong—but they’re often early. His long-term view prioritizes preservation over short-term gains, a strategy that has helped Berkshire weather multiple market cycles.

Similarly, the Federal Reserve has often signaled caution long before market corrections. One of the most famous examples came from Fed Chairman Alan Greenspan, who, during a speech on December 5, 1996, posed the now-famous question:

“How do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions?”

Although widely misquoted at the time, Greenspan’s rhetorical question was interpreted as a warning about overheated markets. Media coverage exploded, with many citing his comment as evidence of a looming crash. But like Buffett, Greenspan’s concern proved accurate just years too early.

A good Op-Ed on Greenspan's speech and the years following is by Alex Pollack, August 16, 2017. He stated,

"When Greenspan gave the speech at AEI, the [NASDAQ] inflation-adjusted index was 1,392, or almost three times as high as the 486 it had been at the end of 1987, his first year in office. That is an average compound annual growth rate of more than 12 percent over nine years—already quite a remarkable run and not sustainable for the long term. But after the speech, to Greenspan’s embarrassment, the market continued its rapid ascent for three more years. By the end of 1999, the inflation-adjusted NASDAQ index was 4,106—three times higher than when Greenspan had issued his warning. At that point, the speech looked pretty bad, to say the least. A few months after that, however, came the top of the market, which had undoubtedly become irrationally very exuberant, then a rapid fall in prices, a dead cat bounce, and then a market collapse. By September 2001, about five years after the speech, real prices were back to where they had been in December 1996. In other words, the inflation-adjusted price gain over nearly five years had been zero. The speech didn’t look too bad when viewed in retrospect from that point. Nonetheless, it had been too early and had backfired as Rubin had predicted. The perfect timing, we can now see, would have been about two years later than the actual speech, at the end of November 1998. Then the warning would have nicely caught the final blow-off and the collapse. When Greenspan retired from the Fed in 2006, the total real price return from a November 1998 warning to his retirement date nine years later would have been zero."

Now the current Federal Reserve Chairman, Jerome Powell, has made history by providing a new warning of overvalued US stocks. During his September 25, 2025, speech in Providence, Rhode Island, the central bank leader was asked how much emphasis he and his colleagues place on market prices and whether they have a higher tolerance for higher values. His response was,

“We do look at overall financial conditions, and we ask ourselves whether our policies are affecting financial conditions in a way that is what we’re trying to achieve. But you’re right, by many measures, for example, equity prices are fairly highly valued."

Clients have been asking whether the current AI-driven tech rally will eventually come to an end. The answer, almost certainly, is yes. History shows that the stronger the gains in prior years, the more dramatic the following correction tends to be — much like Newton’s Third Law of Motion: for every action, there is an equal and opposite reaction. As investor exuberance drives stock prices to unsustainable levels, it’s only a matter of time before valuations revert to historical norms. Unfortunately, that correction is rarely orderly. Once investors recognize that prices have far exceeded realistic levels of earnings, enthusiasm can quickly turn into panic, driving stocks well below their fair value. The good news is that the correction selloff duration is typically 9 to 12 months to the eventual bottom before stocks begin to recover.

It will be essential for investors to take advantage of the current strong market rally. For now, billions of dollars continue to flow into AI infrastructure, fueling a circular economy in which companies generate earnings by selling to one another. Eventually, however, the end users of this technology will need to deliver real profits — and investors will begin demanding tangible returns. This pattern closely resembles the dot-com boom of the late 1990s, when enormous investments flowed into Web-based companies that ultimately failed to produce profits. Mr. Buffett accurately assessed this circular economy starting in 2001:

“The fact is that a bubble market has allowed the creation of bubble companies, entities designed more with an eye to making money off investors rather than for them.”

Stock market bubbles pop when investors lose confidence that companies cannot sustain their torrid business growth. That is typically when the economy and stock market pivot into a Contraction/Assimilation phase, marking the start of a long-term bear market.

Note: I discuss the 130-year unbroken history of repeating 17-year cycles of alternating U.S. Expansion/Growth and Contraction/Assimilation phases in my upcoming second edition of “Physicians Guide to Wealth,” set to be released in October.

One important historical lesson stands out: nearly all the foundational technology developers and manufacturers of the 1990s — such as Intel, Microsoft, AMD, IBM, Google, and Cisco— survived the 2000 market crash. While their stock prices declined sharply, their businesses endured. In contrast, most of the internet-based startups that relied on their technologies went bankrupt.

It’s also worth noting that when market leaders such as Warren Buffett, Alan Greenspan, and Jerome Powell begin to comment on market overvaluation, their warnings tend to be accurate — but early. In my 40 years of experience, these signals typically preceded the actual market peak by two to four years, serving as valuable early indicators for prudent investors.

What Does This Mean for Investors?

Both Buffett’s long-term strategy and the Fed’s cautious remarks highlight a key lesson: while timing the market perfectly is nearly impossible, recognizing signs of unsustainable exuberance is the first step in preparing for change.

At Up Capital Management, our investment approach is centered on momentum confirmation. We conduct daily analysis of economic and market data to assess both the broader environment and underlying trends. However, our primary focus remains on the direction of momentum across stocks and asset classes. No matter how compelling the narrative or data may appear, we wait to invest until a positive trend has been clearly established — and we sell when that trend reverses.

Currently, we maintain a favorable outlook on the U.S. economy and stock market. We believe the positive momentum in leading sectors — particularly technology and large-cap companies — will likely continue into 2026. While we expect some rotation as institutional investors rebalance across asset classes, we anticipate that the market leaders of 2025 will remain at the forefront through 2026.

Let us know if you have any questions about this UPdate. We also welcome the opportunity to discuss strategies for you and your family to achieve your financial wealth-building goals.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions