BLOG

Gambling is not Investing

Throughout my career, I’ve often heard people argue that the stock market is rigged, corrupt, or tilted in favor of wealthy, well-connected investors. Many believe the average individual has little chance of success. Like most generalizations, these comments stray wide of reality.

Having spent nearly 40 years investing in the stock market, I’ve learned not to get worked up too much by these views. That said, it’s fair to acknowledge that there have been and continue to be bad actors on Wall Street and in the public markets. A brief list of well-known individuals convicted of stock market–related fraud includes:

Bernie Madoff– Ran the largest Ponzi scheme in history (about $65 billion). Sentenced to 150 years in prison.

Jordan Belfort– The “Wolf of Wall Street”; involved in stock manipulation and fraud. Served for about 22 months.

Raj Rajaratnam– Hedge fund manager convicted of insider trading (Galleon Group case). Sentenced to 11 years.

Ivan Boesky– 1980s insider trading scandal; cooperated with investigators and served prison time.

Martha Stewart became front-page news amid allegations of insider trading, an activity that members of Congress are permitted to engage in legally. In her case, however, she was not convicted of insider trading but rather of obstruction of justice and making false statements to investigators. The issue arose after she sold her shares, when she misled authorities about the reason for the trade and attempted to conceal that she had received a tip from her broker. That broker was aware that Sam Waksal, CEO of ImClone, was rapidly selling his own shares ahead of an expected negative FDA announcement regarding one of the company’s drugs. Stewart sold 3,928 shares (about $65,000 worth) in 2001, avoiding losses as the stock dropped sharply following the news.

Elizabeth Holmes, the young and charismatic founder of Theranos, rose to celebrity status as her company’s valuation reached $9 billion in 2015. Ms. Holmes, owning roughly half the equity, became one of the youngest female billionaires in history. That success unraveled when it was revealed that she had misled investors about the capabilities of Theranos’ blood-testing technology and the company’s financial condition. She was ultimately convicted of fraud for deceiving investors to secure funding. Theranos collapsed, and Holmes was sentenced in 2023 to 11 years and 3 months in federal prison. The company’s central claim that its technology could run hundreds of accurate tests from a single finger prick proved to be significantly overstated.

For those over 45 or anyone with parents over 55, the skepticism toward the stock market is understandable. Many remember the 1990s explosion of thousands of newly formed dot-com companies, with hundreds going public through IPOs. Leading up to the 2000–2003 market crash, many of these companies had little to no profits, yet their stock prices soared during the boom, making many of their employees overnight millionaires. When reality set in regarding the unsustainability of their business, many companies collapsed into bankruptcy in the early 2000s, along with the finances of their investors and employees.

The fallout was severe in the early 2000’s. Shareholders, retirement accounts like 401(k)s, and employees were hit hard. High-profile cases of corporate fraud, such as Enron and WorldCom, only deepened the damage and discontent, wiping out billions in wealth and eroding public trust.

Even so, these examples represent a small fraction of the broader market. Today, there are more than 4,000 publicly traded companies across U.S. exchanges, representing approximately $45 trillion to $55 trillion in total value. The U.S. remains the dominant force globally, accounting for roughly 40% to 50% of the world’s total stock market capitalization.

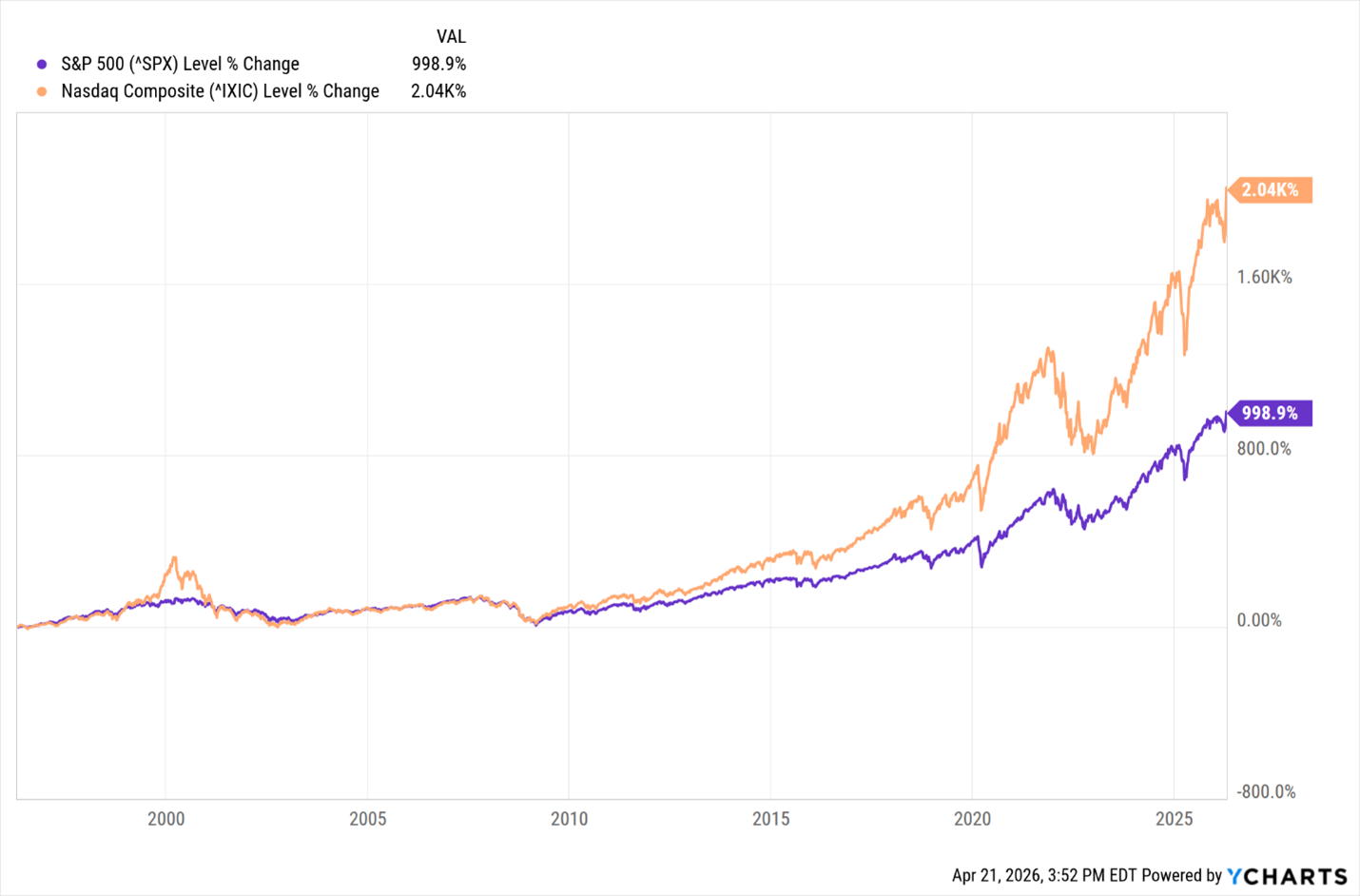

Below are a historical performance outlines and charts of cumulative total return (including dividends) of the S&P 500 and NASDAQ indices for the past 10, 20, and 30 years. Note that one cannot invest directly into an index.

This stands in contrast to the rapidly growing and cleverly branded world of “prediction” markets. Younger generations, who are those below the millennial cohort, are increasingly embracing this form of activity as a type of investment. Their willingness to allocate hard-earned money to these markets is partly driven by a deep skepticism of traditional financial institutions, shaped by watching their parents’ finances suffer through multiple market downturns over the past three decades. As a result, they tend to prioritize present-day experiences over long-term saving and wealth accumulation.

On April 8, 2026, Liz Ann Sonders and Kevin Gordona co-authored a report for Charles Schwab titled "Gambler’s Blues, Betting is not Investing”. In this report, they stated:

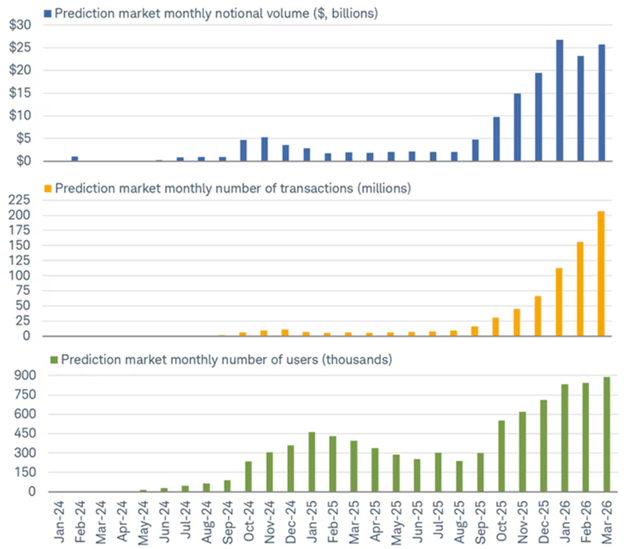

“Prediction markets have grown exponentially, as shown in the chart below. It's not just monthly volume growth, which has risen to more than $25 billion since 2024 according to Dune. It's also total transactions, which have skyrocketed from about 240,000 to more than 200 million, while monthly active users have grown from about 4,000 to almost 900,000 (Dune). At the same time, a March 2026 report from Citizens JMP Securities covering the period from July 2025 to mid-March 2026, showed that prediction market users experienced higher losses than users of other gambling products, with a median loss of 8% compared to a loss of 5% for sports bettors.”

Pete Rose was, in many ways, ahead of his time. Decades after his 1989 lifetime ban from Major League Baseball for betting on games, the landscape shifted dramatically. In May 2018, federal courts struck down the Professional and Amateur Sports Protection Act (PASPA) of 1992, opening the door for states to legalize sports betting.

Since then, the growth of sports wagering, with men accounting for roughly 75% of participants, has been staggering. While the expansion of the industry itself hasn’t been the primary concern for many lawmakers, the real issue lies in the mounting financial losses and, in some cases, the severe economic strain being placed on individuals and families.

In this same report, they reference a UC San Diego Rady School of Management report that studied more than 700,000 online gamblers over five years through 2023, tracking digital payment records across 32 states. The results were alarming but not a surprise to anyone who understands gambling organizations that legally slant the odds entirely in their favor. UC San Diego report stated,

“Researchers found that fewer than 5% of online sports gamblers have withdrawn more money from their gambling apps than they deposited. Let's flip that sentence: More than 95% of participants are net losers over time. This is not a feature of bad luck or poor timing it is the mathematical inevitability built into these products by design.”

Ms. Sonders and Mr. Gordona also referenced a 2024 report by economists Scott R. Baker, Justin Balthrop, Mark J. Johnson, Jason D. Kotter, and Kevin Pisciotta titled "Gambling Away Stability: Sports Betting's Impact on Vulnerable Households”. According to them, this report provides insights into the impact of predictive gambling and the devastation on household finances across America, as most states have embraced this new industry. They quote from this report the following:

“Using transaction data from more than 60 million Americans and analyzing behavior in roughly 230,000 households from 2010 through September 2023, the researchers explored the staggered state-by-state legalization of online sports betting following the Supreme Court's 2018 ruling to isolate the causal impact of gambling access on financial outcomes.

The findings are jarring. When online sports betting became available in a state, participation spread quickly and it did not slow down. Users who were net losers did not gradually learn their lesson and step back; instead, they bet more. The research found not only an expansion among new users, but a pattern in which losing participants increased their wagering over time, a dynamic consistent with the addictive behavioral profile these platforms are designed, consciously or not, to cultivate.

Critically, the increase in gambling spending did not come at the expense of other entertainment, e.g., dining, concerts, or existing lottery and poker spending. It came at the expense of savings and investment. For every dollar directed toward sports betting, net investment in equities and other financial instruments fell by just over two dollars. The money flowing into these gambling sites was not discretionary leisure spending. It was likely wealth that would otherwise have been building toward long-term financial security”[emphasis added]

What Does This Mean to Me?

The key distinction between gambling and investing is simple: gamblers are hoping, while investors are owning. Gamblers have no ownership in what they are betting on and no control over the outcome or odds. Once a bet is placed, the result is final, and there’s no opportunity to recover losses except by placing another bet. Each wager is a short-lived, one-time event.

Investors, on the other hand, own a piece of the companies they invest in. While stock prices may fluctuate, businesses with strong, profitable models and valuable products or services can generate meaningful long-term returns.

Warren Buffett, co-founder and longtime Chairman of Berkshire Hathaway, is well known for committing large amounts of capital to a select group of companies and holding them through economic cycles. Berkshire’s long-term holdings have included American Express (1960s), GEICO (1970s), Coca-Cola (1988), Bank of America (2011), Apple (2016), and Chevron (2020).

As noted earlier, long-term returns have been earned simply by investing in the S&P 500, which represents many of the largest U.S. companies. For most investors, success comes not from timing the market but from time in the market. Investors also have a wide range of strategies to manage their portfolios, and unlike a bet, their ownership does not expire as they can buy, hold, or sell during market hours. Ultimately, the stock market rewards those who are informed, disciplined, and patient, as is true in most legitimate fields where knowledge and experience matter.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions