BLOG

Building and Preserving Wealth

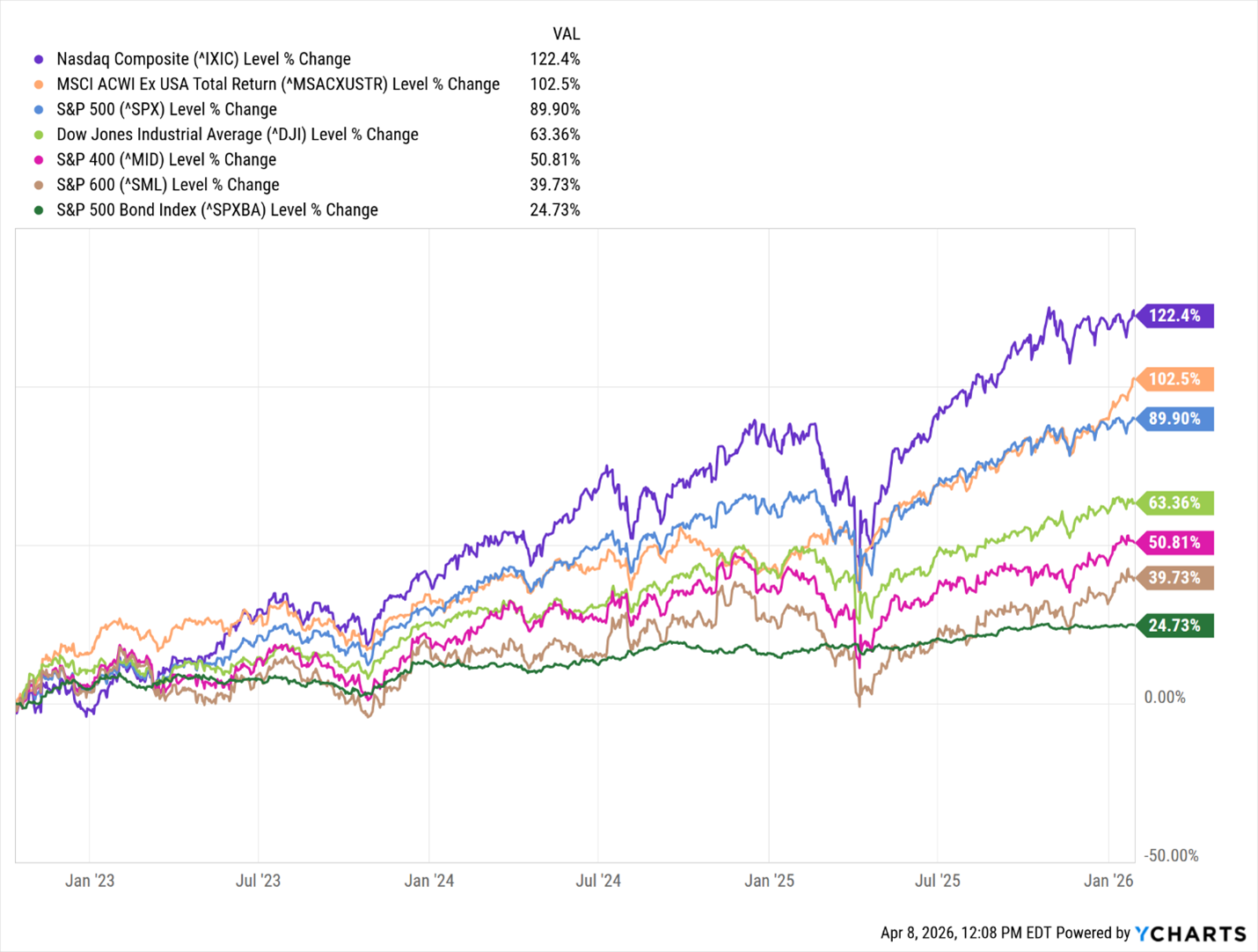

From October 13, 2022, U.S. equities embarked on a powerful rally, with the S&P 500 and Nasdaq outperforming most global indices through January 29, 2026. However, as reports of a potential conflict with Iran began to surface early this year, growing fears of war started to weigh on investor sentiment and pressure the markets.

Below is an outline of the returns of these indices from October 13, 2022, to January 29, 2026

NASDAQ:122.40%

MSCI Ex US:102.50%

S&P 500:89.90%

Dow Jones Industrial Average:63.36%

S&P 400 Mid Cap:50.81%

S&P 600 Small Cap:39.73%

S&P Bond:24.73%

The MSCI Ex US index had been lagging or matching the gains of the S&P 500 until December 29, 2025, when it broke to the upside and surpassed the S&P 500. Also, notice the significant underperformance of the S&P 400 (mid-cap) and S&P 600 (small-cap) indices during this period. These two indices have been trailing the S&P 500 since 2018, and the longest period I can recall for small and mid-caps to trail the large-cap sector.

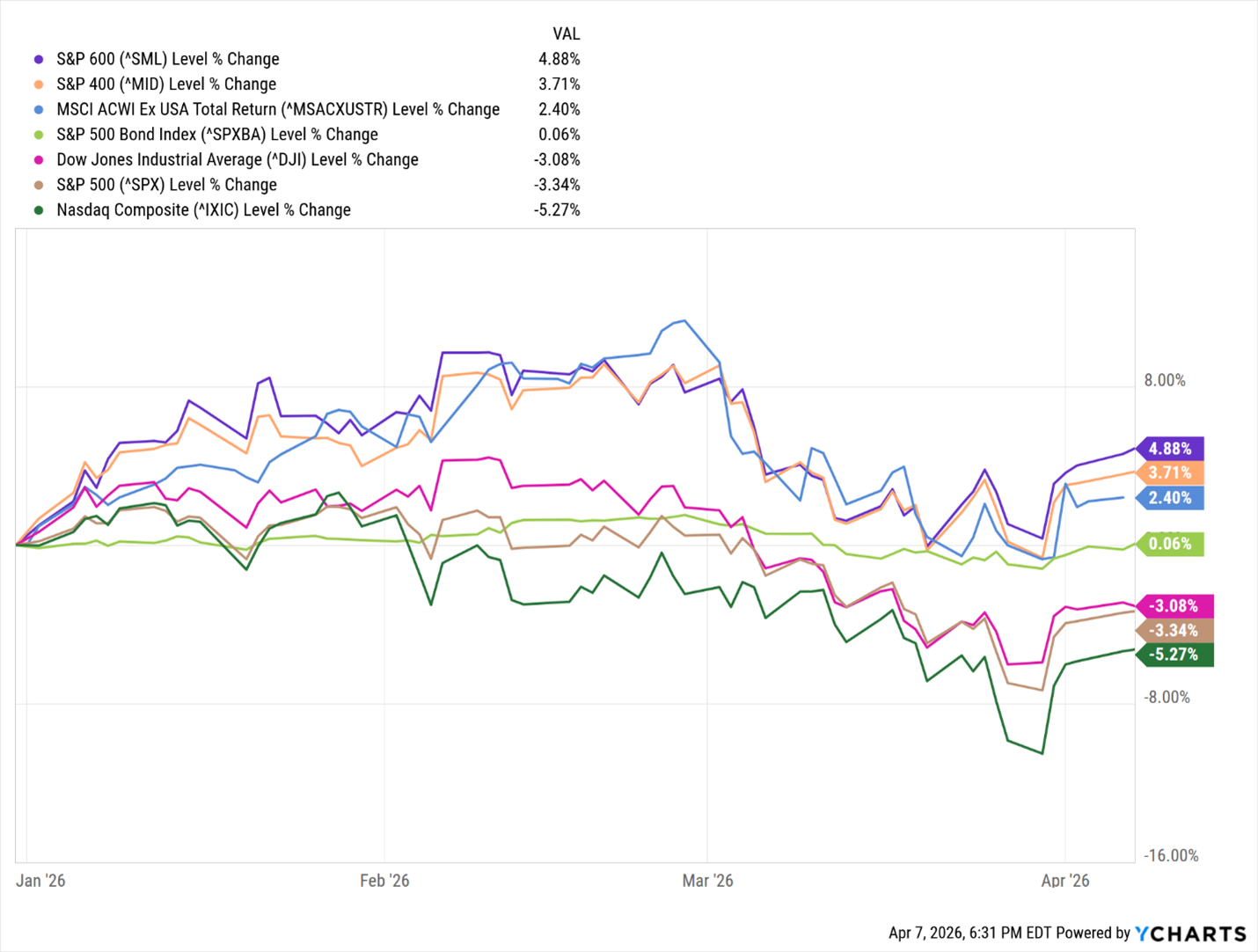

However, since January 1, 2026, the leadership of these indices has finally reversed. The YTD returns of the S&P 600 is 4.88%, and the S&P 400 is 3.71% compared to losses for the S&P 500 and NASDAQ OF -3.34% and 5.27%, respectively.

Since late January, major indices have drifted lower, with selling pressure accelerating after February 28 as the conflict with Iran intensified. What caught many investors off guard this year was the aggressive selling of gold, silver, and mining stocks by institutional investors that had performed exceptionally well in 2025. Conventional thinking would suggest increasing exposure to precious metals as rumors of war escalated. Yet, as fears of war grew, gold and silver defied historical patterns and fell nearly 20% during February and March. As mentioned in prior Updates, we sold our mining stocks earlier this year with nice profits, with most of the proceeds being held in cash equivalent funds.

Many clients have asked how I’ve handled the past several months, marked by market declines, heightened volatility, and uncertainty. Candidly, I experience more stress during prolonged rallies than during corrections. After more than 28 years of managing portfolios, I know every rally eventually ends. During uptrends, I’ve been successful in identifying opportunities and participating in rising markets, adding to our portfolios companies like Nvidia in 2022 at $19 per share (now around $178), along with past profitable positions in Home Depot, Apple, Dick’s Sporting Goods, Hilton, Chipotle, Michael Kors, Gap, and others. Managing the growth portion of the portfolio during uptrends is a constant process of adding capital to the strong momentum stocks or indices and trimming or selling the underperforming ones.

However, what concerns me most is the reversal and how to navigate a downturn to limit losses. While I know rallies don’t last forever, the key unknowns are timing, cause, depth, and duration of market trend reversals. I’m not referring to brief pullbacks or short-lived disruptions, like last April’s tariff-driven market crash, which tends to create temporary buying opportunities within an ongoing uptrend.

The real challenge is when an uptrend ends and transitions into a prolonged flat or declining market. Our priority is not only to build wealth for clients, but to preserve it. There’s little value in years of gains if portfolios ultimately fall back to prior levels. It’s not just about what you make, it’s about what you keep.

When a sustained uptrend breaks down, managing risk becomes significantly more complex. Bear markets can last months or even years, often with no clear signal of when a bottom has been reached. It can feel like navigating an aircraft with engine trouble; it’s not if we are landing, it’s where and with the least amount of damage.

Equally difficult is identifying the right moment to re-enter a new uptrend. Missing the bottom and waiting too long can mean missing a powerful recovery. Early in rebounds, analysts often remain cautious, warning of new risks that prompt less experienced or unaware investors to not reinvest.

We saw this in October 2022, when markets began a multi-year rally despite widespread recession warnings. Similarly, after the March 24, 2020, bottom, many analysts expressed extreme caution to investors, citing yield curve inversion (when short-term rates are higher than long-term rates), supply chain issues, dysfunction among governments, health risks, and other indicators to signal greater downside risks. Yet institutional investors aggressively invested back into the stock market while the cautious and timid investors remained on the sidelines and missed a huge stock market rally that continued climbing for nearly two years into early 2022.

Since October 28, 2025, major U.S. indices have traded within a relatively flat range. Then, as noted, selling began in late January 2026, pulling down both indices and many leading stocks. The conflict with Iran and the closure of the Strait of Hormuz created significant supply chain disruptions, along with rising shortages of oil and gas. In response, we maintained unusually high cash allocations this year in our Growth & Income and Growth portfolios as a hedge against downside risk amid increasing volatility.

Last week, we rebalanced these portfolios, redeploying cash back into equities, including mining stocks, a move that has proven timely. Yesterday, President Trump announced a two-week ceasefire agreement with Iran and the reopening of the Strait of Hormuz. Today, our growth allocations are performing well as U.S. and global markets are responding with a strong surge in buying activity.

What Does This Mean to Me?

Managing investment portfolios is a continuous process that often requires daily and at times hourly monitoring of political developments, economic data, and market trends. Remaining competitive and outperforming benchmarks depends on recognizing and responding to key shifts in markets and the broader economy. President Trump has added another layer of complexity with aggressive and sometimes abrupt policy decisions, similar to the challenges we experienced during his first administration, as noted in our prior UPdates.

So far this year, we have focused on minimizing downside risk and avoiding many of the significant drawdowns in individual stocks. We also anticipated a market rebound tied to progress toward resolving the conflict with Iran and the reopening of the Strait of Hormuz.

Looking ahead, once a more durable resolution with Iran is achieved and the initial relief rally subsides, investors will begin assessing whether a new sustained uptrend is forming. Key factors we are monitoring include the trajectory of oil prices and, particularly whether they return to pre-conflict levels. In addition, we are most concerned with the direction of interest rates and inflation. We are also monitoring the appointment of the next Federal Reserve Chair and the policy direction that follows. Meanwhile, consumer sentiment remains near historically low levels, dating back to records beginning in 1957.

For now, we are encouraged by the de-escalation and relieved for the people and families in Iran who were at serious risk as the regime forced them to stand around power plants and bridges.

We are also satisfied with last week’s portfolio rebalancing and the opportunity it has created for our clients to benefit from today’s market rebound.

CONTACT

Check the background of your financial professional on FINRA's BrokerCheck.

The content is developed from sources believed to be providing accurate information. The information in this material is not intended as tax or legal advice. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.

We take protecting your data and privacy very seriously. As of January 1, 2020 the California Consumer Privacy Act (CCPA) suggests the following link as an extra measure to safeguard your data: Do not sell my personal information.

The information on this website is the opinion of Up Capital Management and does not constitute investment advice or an offer to invest or to provide management services. Before purchasing any investment, a prospective investor should consult with its own investment, accounting, legal, and tax advisers to evaluate independently the risks, consequences, and suitability of any investment.

Copyright 2024 | Privacy Policy | Terms & Conditions